A year like no other, 2020 has presented many unexpected challenges. Projecting overall insurance premiums and losses in the current pandemic environment is one such challenge, especially for workers compensation (WC). Premium for this line of business is particularly sensitive to changes in employment and payroll, and WC losses have been impacted by temporary pandemic-related business closures.

This article is a supplement to the

2020 Workers Compensation Financial Results Update published in October 2020 and contains countrywide private carrier WC premium and combined ratio estimates for Calendar Year 2020.

Key Takeaways

While still preliminary, our countrywide analysis shows:

- WC Calendar Year 2020 private carrier net written premium is estimated to be $38.6 billion. This represents an 8.1% decline when compared with Calendar Year 2019.

- The WC private carrier combined ratio for Calendar Year 2020 is estimated to be 86%, compared with an 85% combined ratio for the prior year.

The extent of the actual Policy Year 2020 premium decline may not be known until well into 2021, after all premium audits on policies effective in 2020 have been completed. As detailed in

COVID-19, Premium Audits, and EBNR - Lessons Learned from the Past, if carriers do not adjust their historical earned but not reported (EBNR) premium estimates to account for the increase in audit-return premium that will likely occur on policies effective during 2020, then Calendar Year 2020 premium and combined ratio results may appear better than they should. Further, the residual effects of the change in audit-return premium on results may linger into 2021—possibly causing Calendar Year 2021 combined ratio results to appear worse than they otherwise would have been absent a change in audit premium.

Countrywide Private Carrier Written Premium

All else equal, countrywide WC premium is expected to decline due to the overall average impact of decreases in rates/loss costs approved by state insurance departments effective in 2020. Changes in rates/loss costs are reflective of several factors that impact system costs, such as changes in the economy, cost containment initiatives, and reforms. In addition, pandemic-related declines in employment and payroll during 2020 are expected to further reduce overall WC premiums.

On a countrywide basis, NAIC private carrier direct written premium (DWP) declined 8.1% through the first three quarters of 2020 compared with DWP through the first three quarters of 2019. The table below summarizes the cumulative DWP changes through the first, second, and third quarters of 2020 compared with the same time periods in 2019.

The large number of pandemic-related job losses that occurred in Second Quarter 2020 accounts for most of the 8.0% premium decline observed when comparing premium through Second Quarter 2020 to premium through Second Quarter 2019.

An alternate approach for estimating the change in 2020 DWP is to combine estimated changes for the individual premium-related components of employment, wages, and rate/loss costs.

- Compared with 2019, private employment in NCCI jurisdictions declined by 5.1% in the first three quarters of 2020. Further, NCCI’s

Quarterly Economics Briefing (QEB)Employment Scenario Tool estimates a –3.7% to –5.1% employment decline from Fourth Quarter 2019 to Fourth Quarter 2020.

- As 2020 employment losses have been largely concentrated in low-wage jobs and sectors, total employment has declined more rapidly than payroll.

Average weekly earnings continued to rise in 2020—by 5.3% on a countrywide basis.

-

The average impact of approved 2020 rate/loss cost filings in NCCI jurisdictions is –7.2%.

All else equal, these component changes in combination suggest an overall change in DWP for NCCI jurisdictions of approximately –7%. Because the 2020 countrywide employment decline has been about one percentage point larger than that for NCCI jurisdictions, this estimate is closely aligned with the reported changes in countrywide private carrier DWP to date.

Quarterly NAIC Annual Statement data does not include net written premium (NWP) information. Given the timing of the pandemic, we assumed that reinsurance for 2020 policies was already in place and therefore the relationship between NWP and DWP in 2020 would be consistent with the prior year. Therefore, it is reasonable to believe that the countrywide change in DWP is an appropriate proxy for the countrywide change in NWP.

Assuming the change in premium through the first three quarters of 2020 is indicative of what we may expect through the end of 2020, our current countrywide private carrier NWP estimate for Calendar Year 2020 is $38.6 billion. This represents an 8.1% decline when compared with Calendar Year 2019.

Countrywide Private Carrier Combined Ratio

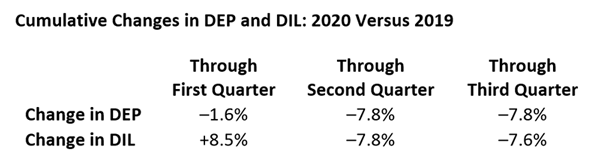

The table below summarizes cumulative changes in countrywide private carrier direct earned premium (DEP) and direct incurred losses (DIL) through the first, second, and third quarters of 2020 compared with the respective time periods in 2019. DEP declined 7.8% through the first three quarters of 2020 compared with the first three quarters of 2019. DIL declined similarly (–7.6%) over this same time period—although the cumulative changes in DIL throughout the year were relatively more volatile.

As mentioned above, pandemic-related factors account for most of the observed decline in premium when comparing Second Quarter 2020 to Second Quarter 2019. With respect to losses, NCCI surveyed more than 25 of the largest private WC carriers to gather pandemic-related, qualitative information. In general, the information suggested that decreases in non-COVID-19 loss dollars appear to have more than offset increases directly attributable to the COVID-19 virus. These survey results are consistent with the decline in incurred losses observed during Second Quarter 2020. Since that time, as the economy began to show signs of recovery, cumulative changes through Third Quarter 2020 appear to have stabilized.

The countrywide combined ratio is calculated as the sum of losses and expenses divided by premium. Consistent with NWP, quarterly NAIC Annual Statement data does not include net earned premium (NEP) or net incurred losses (NIL). As such, we have assumed the Calendar Year 2020 changes in NEP and NIL will equal the cumulative changes in DEP and DIL, respectively, through Third Quarter 2020. Further, because the quarterly NAIC data does not contain expenses by line of business, we have assumed that WC expense ratios for 2020 will be equal to those for 2019.

NCCI estimates that the overall WC private carrier combined ratio for Calendar Year 2020 will be 86%, compared with an 85% combined ratio for the prior year. The following chart shows a history of calendar year private carrier combined ratios along with the 2020 estimate.

NCCI will share its updated estimates for 2020 at

AIS 2021—Stronger Together, scheduled for May 11–12, 2021.

Notes

This document includes assumptions and projections. As with any prospective analysis, there exists estimation uncertainty in these assumptions and projections. Areas of this analysis subject to estimation uncertainty that could have a material impact on the results include:

- Fourth Quarter 2020 DWP, DEP, and DIL changes

- The relationship between direct and net business

- The expected expense ratios

- The impact of changes to laws and regulations

This article is provided solely as a reference tool to be used for informational purposes only. The information in this article shall not be construed or interpreted as providing legal or any other advice. Use of this article for any purpose other than as set forth herein is strictly prohibited.