When thinking about COVID-19 and premium audits, our first thoughts go to the challenges auditors may have with in-person audits and staying safe. While worker safety is always the paramount consideration, our subject today is about a related issue—the accuracy and timeliness of the financial estimates carriers are required to make for the premium these audits generate.

This financial estimate, known as Earned but Not Reported premium (EBNR), is the premium counterpart to the better-known Incurred but Not Reported component of loss reserves (IBNR). The difference is that EBNR is an asset, whereas IBNR is a liability. EBNR has always been important but is generally less impactful than IBNR.

While not common, IBNR changes may affect industry results from time to time as insurers routinely review and adjust their loss reserves. On the other hand, EBNR can go for long periods without a deep review due to the stability in audit premiums. With the current recession underway, leaving the EBNR assumptions unchanged can be impactful—and sometimes in surprising ways.

Premium billing lags can contribute to EBNR (which is why it is also called Earned but Unbilled premium or “EBUB”), but the greatest impact in workers compensation insurance comes from payroll audits. When audited payroll is larger than the up-front estimated payroll, additional premium due results at audit. The opposite results in a return of premium to the insured at audit. Usually, the audit-additional premiums are fairly stable, but when a recession strikes, this may change.

The chart below shows the stability of audit premium during normal times but highlights the swing in audit premium associated with a recession—as audit premium goes from net additional premium to net return premium due to the contraction in actual payroll during the economic downturn.

We can look at the Great Recession to see what happens when EBNR revisions are delayed due to changing economic conditions. If the EBNR revisions recognize the swing from audit-additional premiums to audit-return premiums in a timely fashion, the economic impact on premium will be reflected in the appropriate calendar year. The negative EBNR correctly anticipates return premium, and the impact is accounted for in the year in which the EBNR is revised. Then, when premium is returned to the insured at audit (as anticipated by the EBNR reserve), the impact on the premium reserves will be offset.

However, if the EBNR is not revised, and is anticipating audit-additional premium notwithstanding the likely audit-return premium that will occur, the results will be distorted by year—initially appearing better than they should, only to have worse results when the audit-return premium is eventually processed.

One can think of the EBNR reserve at a policy level. When the audit-return premium is processed, the EBNR reserve, which anticipated that return would be released, and the net impact will be zero. This is similar to a loss reserve on a claim which correctly anticipates the timing of the eventual claim payments. The impact of establishing a loss reserve on calendar year results occurs when the reserve is established. If the reserve is accurate, there is no further impact on incurred losses when the associated claim payments are made.

A delay in revising EBNR reserves may be compounded when the initial estimated premium on renewal policies reflects the lower actual payroll observed on expiring policies (i.e., those policies associated with the audit-return premium). In the same period that audit-return premiums are being processed on expiring policies, the expected premium on the renewal policies will also be lower. Therefore, written premium for that calendar period will look extra low since high-payroll estimates in the prior policy period are being corrected over and above the decline in actual insured policy payroll volume attributable to economic conditions—a double whammy, as two years of impacts are rolled into one. This affects both written and earned premium.

NCCI’s loss cost filings are based on policy year premium and loss experience.1 While policy year premium may be impacted by changes in economic conditions, the definition of policy year premium ensures that the impact of a premium audit is accounted for in the year when the policy becomes effective. However, when calendar year premium is used (such as in GAAP income statements), timing issues may arise.

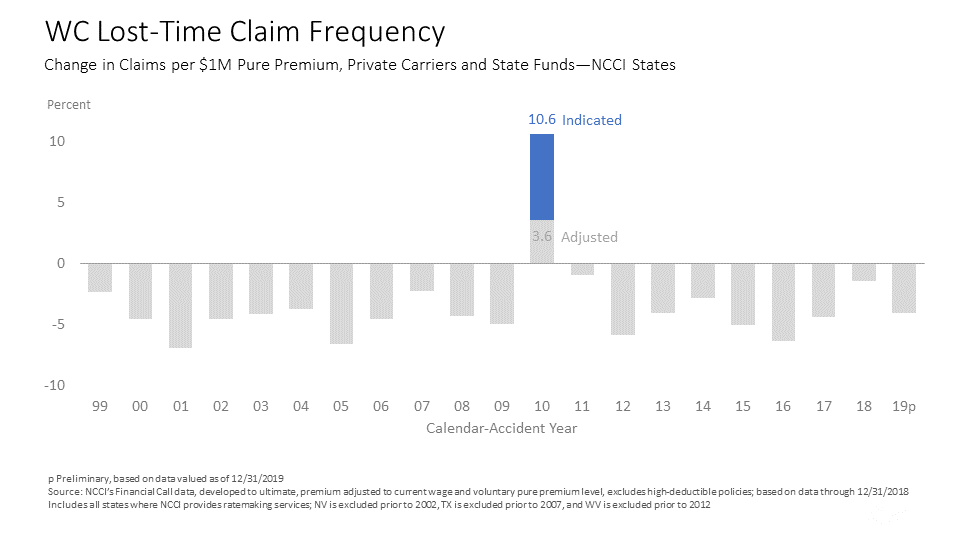

NCCI uses calendar-accident year (CAY) data for our claim frequency analysis. Claim frequency is defined as the number of lost-time claims per $1M of pure premium at current wage and voluntary loss cost level. Calendar year refers to the premium in the denominator and accident year refers to the claim counts in the numerator. As the chart below shows, claim frequency results were generally stable during the Great Recession. When we thought we were out of the recession, frequency in 2010 jumped more than 10 points.

It turns out that many carriers did not update their EBNR in 2008 or 2009. Premium distortions worth 6% of Calendar-Accident Year 2010 premium were manifesting. The more than 10-point jump in claim frequency mentioned above was overstated by 6 points. After also accounting for an industry group mix change, the true 2010 claim frequency increase was approximately 3.5 points. This is just a timing issue; besides adjustments to 2010, there were smaller offsetting adjustments to prior years and no net change over the multiyear period. In addition, earned premium is also impacted and causes calendar-accident year loss ratios to appear worse.

The good news is that carriers are aware of this issue and many are undertaking EBNR reviews right now. It is early and account information is limited, but even with the current economic uncertainty, it is usually clear which direction EBNR needs to move. There is no doubt that times are tough for employers and that the impact of the current recession may last longer than thought earlier this year. However, we have learned from the last recession. Hopefully, we will emerge from this one with the issue of audit-return premiums’ impact on calendar-accident year results behind us, and the results for the first post-recession year will not be clouded by an EBNR hangover.

This article is provided solely as a reference tool to be used for informational purposes only. The information in this article shall not be construed or interpreted as providing legal or any other advice. Use of this article for any purpose other than as set forth herein is strictly prohibited.