At its Annual Issues Symposium (AIS) in May 2020, NCCI presented the State of the Line Report—a comprehensive account of financial results for the workers compensation (WC) line of business. The results presented reflected the most up-to-date data available at the time, including NCCI’s preliminary estimates for Calendar Year 2019. In this report, NCCI provides updated results for 2019.

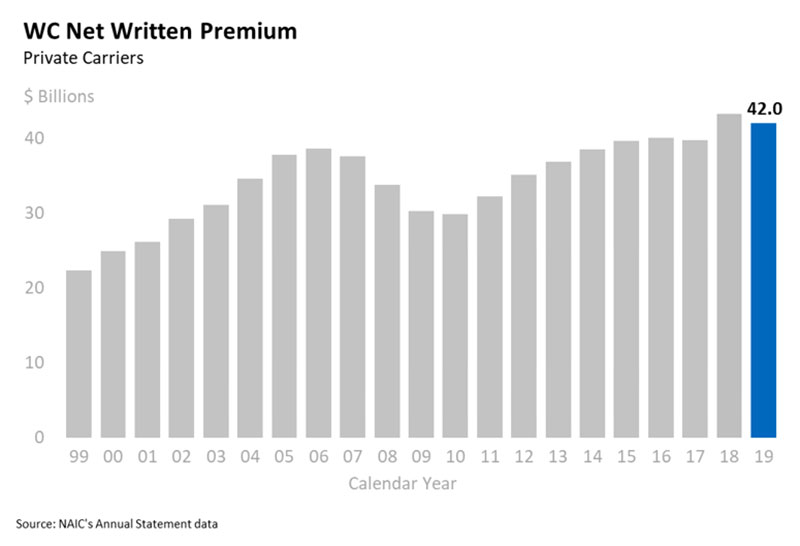

For Calendar Year 2019, NCCI estimated WC premium volume net of reinsurance to be $42.0 billion for private carriers. This is consistent with the most recently reported industry data for that year and represents a 3% decrease in net written premium (NWP) versus 2018. Prior to 2018, increased utilization of offshore reinsurance stalled NWP growth. Driven by the additional tax burden on business transferred to offshore affiliates imposed by the Base Erosion and Anti-Abuse Tax (BEAT) provision of the Tax Cuts and Jobs Act of 2017, NWP grew by $3.5 billion in 2018. While the BEAT’s residual effect and the strong economy placed upward pressure on 2019 NWP, the recent decreases in rates/loss costs more than offset these factors.

Changes in rates/loss costs impact premium growth and are reflective of several factors that impact system costs, such as changes in the economy, cost containment initiatives, and reforms. NCCI expects premium in 2020 to decrease by 7.2%, on average, as a result of rate/loss cost filings made in jurisdictions for which NCCI provides ratemaking services. The cumulative decrease since 2004 is 44%. Improved experience driven by declines in lost-time claim frequency has contributed to this cumulative decline. The changes shown below reflect both voluntary and assigned risk market approvals.

For Calendar Year 2019, NCCI estimated a WC net combined ratio of 85% for private carriers. The updated data reported by the industry indicates a private carrier 2019 combined ratio of 85.4%, which translates to an underwriting gain of 14.6%. The 2019 combined ratio is the second lowest combined ratio in recent history and the sixth consecutive underwriting gain for the industry.

The WC investment gain on insurance transactions (IGIT) measures investment performance by comparing investment income allocated to the WC line of business with the corresponding earned premium. At AIS 2020, the IGIT for Calendar Year 2019 was estimated to be 11% of net earned premium. The updated data reported by the industry indicates a ratio of 10.6%. This latest gain is still below the 12.6% long-term average since 1999.

The WC pretax operating gain measures the overall financial performance of the WC line of business, reflecting both underwriting and investment income. The 2019 underwriting gain of 14.6%, combined with the investment gain of 10.6%, resulted in a WC operating gain of 25.2%. This value is slightly lower than the preliminary estimate of 26% shared at AIS 2020 and marks the third consecutive operating gain exceeding 20% for the industry.

Typically, NCCI would have included preliminary estimates of the 2020 combined ratio and net written premium volume in this report. Due to the uncertainties surrounding the ongoing COVID-19 pandemic, including its direct and indirect effects on WC premium and losses, NCCI will be sharing more insights for 2020 in the coming months.

This article is provided solely as a reference tool to be used for informational purposes only. The information in this article shall not be construed or interpreted as providing legal or any other advice. Use of this article for any purpose other than as set forth herein is strictly prohibited.