At its

Annual Issues Symposium (AIS) in May 2021, NCCI presented the

State of the Line Report—a comprehensive account of financial results for the workers compensation (WC) line of business. The results presented in that report reflected the most up-to-date data available at the time, including NCCI’s preliminary estimates for Calendar Year 2020. In this report, NCCI provides updated results for 2020 as well as preliminary information for 2021.

Key Takeaways

The final countrywide analysis shows:

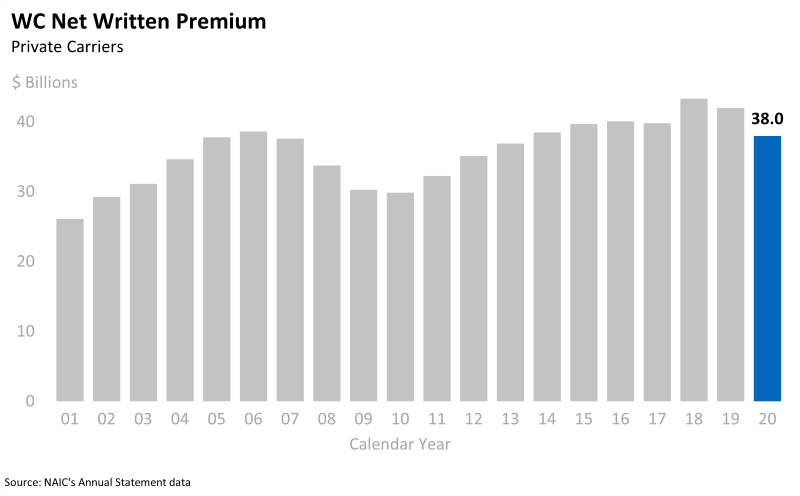

- WC Calendar Year 2020 private carrier net written premium (NWP) decreased from 2019 by 9.5% to $38.0 billion

- The WC Calendar Year 2020 private carrier combined ratio was 87.0% and the operating gain was 23.2%

While still early and subject to revision, preliminary analysis through the second quarter of 2021 shows:

- WC Calendar Year 2021 private carrier direct written premium (DWP) declined through the first two quarters of 2021, compared with DWP through the first two quarters of 2020

- The WC Calendar Year 2021 private carrier direct loss ratio through the first two quarters of 2021 is similar to that observed through the first two quarters of 2020

WC Net Written Premium

For Calendar Year 2020, NCCI estimated WC premium volume net of reinsurance (NWP) to be $38.0 billion for private carriers. This is consistent with the most recently reported industry data for that year and represents a 9.5% decrease versus 2019’s NWP volume of $42.0 billion.

On a policy year basis, the extent of the actual 2020 premium decline is still unknown because premium audits on policies effective in 2020 are still ongoing. Audit-return premium will likely occur to some extent on policies effective during 2020 due to the observed payroll declines associated with the COVID-19-related economic recession. To the extent that carrier earned but not reported (EBNR) premium estimates do not fully account for this,1 it is possible that premium volume and combined ratio results for Calendar Years 2020 and 2021 may be affected. In other words, it is possible that the Calendar Year 2020 results may appear better and those for Calendar Year 2021 may appear worse than they otherwise would have, in the absence of a change in the historical audit premium pattern.

WC Financial Results

For Calendar Year 2020, NCCI previously estimated a WC net combined ratio of 87% for private carriers. The updated data reported by the industry indicates no change from that estimate. The 87% combined ratio represents a 13% underwriting gain.

The 2020 combined ratio is the third lowest combined ratio in recent history and the seventh consecutive underwriting gain for the industry. The current period of consecutive underwriting gains is unprecedented in terms of both duration and magnitude.

The WC investment gain on insurance transactions (IGIT) measures investment performance by comparing investment income allocated to the WC line of business with the corresponding earned premium. At

AIS 2021, the IGIT for Calendar Year 2020 was estimated to be 11% of net earned premium. The updated data reported by the industry indicates a ratio of 10.2%. This latest gain is below the 12.2% long-term average since 2000.

The WC pretax operating gain measures the overall financial performance of the WC line of business, reflecting both underwriting and investment income. The 2020 underwriting gain of 13.0%, combined with the investment gain of 10.2%, resulted in a WC operating gain of 23.2%. This value is slightly lower than the preliminary estimate of 24% shared at

AIS 2021 and marks the fourth consecutive operating gain exceeding 20% for the industry.

Preliminary 2021 Analysis

Changes in rates/loss costs impact premium growth and are reflective of several factors that impact system costs, such as changes in the economy, cost containment initiatives, and reforms. All else equal, NCCI expects premium in 2021 to decrease by 5.6%, on average, as a result of rate/loss cost filings made in jurisdictions for which NCCI provides ratemaking services. Improved experience driven by declines in lost-time claim frequency has contributed to this decline. The changes shown below reflect both voluntary and assigned risk market approvals.

On a countrywide basis, NAIC private carrier DWP declined 1.6% through the first two quarters of 2021, compared with DWP through the first two quarters of 2020. The table below summarizes the cumulative DWP changes through the first and second quarters of 2021, compared with the same time periods in 2020.

As mentioned above, premium audits may be affecting the reported written premium totals.

Quarterly NAIC Annual Statement data does not include NWP information. Assuming changes in Calendar Year 2021 DWP and NWP will be similar and DWP volume will increase during the second half of 2021 relative to the second half of 2020, it is reasonable to expect, at this point, that the WC Calendar Year 2021 countrywide private carrier NWP total may be close to the $38.0 billion figure observed for 2020.

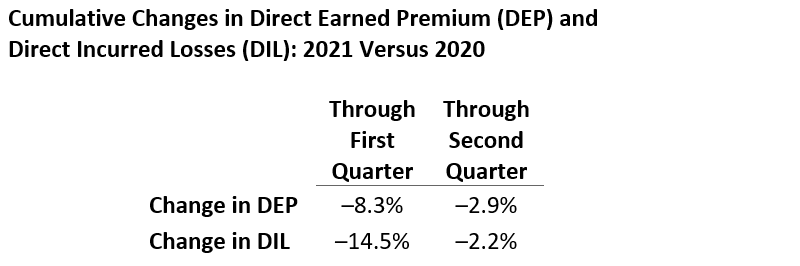

The countrywide combined ratio is calculated on a direct basis as the sum of losses and expenses divided by premium. The largest components of the combined ratio are the direct earned premium (DEP) and direct incurred losses (DIL). The table below summarizes cumulative changes in countrywide private carrier DEP and DIL through the first and second quarters of 2021, compared with the respective time periods in 2020. DEP declined 2.9% through the first two quarters of 2021 compared with the first two quarters of 2020, and DIL declined similarly (–2.2%) over this same time period.

As with NWP, quarterly NAIC Annual Statement data does not include net earned premium (NEP) or net incurred losses (NIL). As such, we have assumed for the sake of this analysis that the Calendar Year 2021 changes in NEP and NIL will approximately equal the cumulative changes in DEP and DIL, respectively, and that the changes in DEP and DIL will be similar to each other in magnitude through year-end 2021. Further, because the quarterly NAIC data does not contain expenses by line of business, we have assumed for the sake of this analysis that WC expense ratios for 2021 will be equal to those for 2020.

Based on these assumptions, NCCI estimates that the countrywide WC Calendar Year 2021 private carrier combined ratio will be similar to the 2020 combined ratio of 87%. NCCI will share its updated estimates for 2021 at AIS 2022, scheduled for May 9–11, 2022.

Notes

This document includes assumptions and projections. As with any prospective analysis, there exists estimation uncertainty in these assumptions and projections. Areas of this analysis subject to estimation uncertainty that could have a material impact on the results include:

- Third and Fourth Quarter 2020 DWP, DEP, and DIL changes

- The relationship between direct and net business

- The expected expense ratios

- The impact of changes to laws and regulations

This article is provided solely as a reference tool to be used for informational purposes only. The information in this article shall not be construed or interpreted as providing legal or any other advice. Use of this article for any purpose other than as set forth herein is strictly prohibited.