This article is Part 2 of a study focusing on automation. Read

Part 1 for historical context and an explanation of why automation in the future has the potential to change labor markets more dramatically than in the past.

The previous edition of the

Quarterly Economics Briefing (QEB) looked at how technological change has impacted the labor market historically, and reviewed several recent studies that try to quantify the potential impact of automation on employment in the future.

Two of the most widely cited studies, one by the McKinsey Global Institute1 and another by Oxford University researchers Carl Frey and Michael Osborne2, start by analyzing the ability to automate specific tasks and build up to estimates of ability to automate different occupations and entire sectors of the economy. Importantly, both studies focus on

automation potential. They ask how much labor currently required to perform various tasks or occupations might feasibly be automated with existing technology. But these studies, as well as others like them, stop short of suggesting how quickly the potential for automation might be realized, or how labor markets might change as a result.

In this edition, we develop scenarios to evaluate the impact on labor markets and employment of different rates of

automation penetration, by which we mean the degree to which automation potential across different economic sectors is realized in the future. We will address these questions:

- What occupations and economic sectors face the largest potential employment impacts from automation?

- What factors besides technical potential might determine the speed of automation penetration?

- What are the implications for workers compensation of shifts in the composition of the workforce induced by automation?

Finally, we will look beyond our scenarios to speculate about how automation might affect employment at a macro-economic level. This raises the difficult question of whether labor productivity gains due to automation will reduce the demand for employment overall, or whether new types of jobs will evolve to replace old jobs lost to automation.

A Baseline Scenario for Automation Penetration

We will first create a framework to illustrate how much automation could affect total employment in different sectors of the US economy. To start, we merge the most recent projections of future employment and output from the Bureau of Labor Statistics (BLS) for the 10 years from 2014 to 2024 with sector-level estimates of automation potential from the McKinsey study. We can then construct scenarios to estimate how many workers in each economic sector could be displaced at different levels of automation penetration. In order to link automation penetration to employment, we need to answer these questions:

- How does automation penetration translate into labor productivity gains—allowing a given amount of output to be produced with less labor?

- How much automation penetration is already “baked into” the BLS projections?

Automation and Labor Productivity

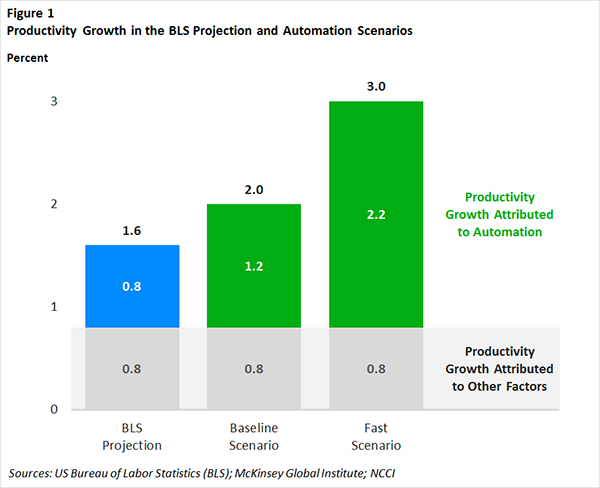

Labor productivity tends to increase over time, both because of major technological breakthroughs as well as ongoing marginal improvements to existing processes and procedures, capital accumulation, and other factors3. Over the last 50 years, US labor productivity has grown at an average of about 1.8% per year. The McKinsey study produced a range of estimates suggesting that automation will contribute 0.3% annually to labor productivity growth in its slowest adoption scenario and 2.2% in its most aggressive.

BLS projects labor productivity growth to be about 1.6% annually over the 10 years from 2014 to 2024. This is slightly lower than the long-term average but would be a rebound from the slow annualized productivity growth of 1.1% since the Great Recession4. BLS does not specify exactly how much of labor productivity will be due to automation, but it is one factor explaining why it projects labor productivity growth to be higher in the

next 10 years than in the

last 105. As a working assumption, we assign half of the gain in each sector to automation and half to other factors—about 0.8% each economy-wide.

With this assumption, automation’s contribution to labor productivity growth in the BLS projections falls on the conservative side of McKinsey’s estimated range of potential growth rates, but not all the way at the lower edge. We will develop two scenarios, as shown in Figure 1, in which we assume greater automation penetration and associated increased labor productivity. These scenarios bring labor productivity growth above long-term averages but not outside the bounds of possibility. In both scenarios, we will assume that other factors affecting labor productivity besides automation do not change when we change the rate of automation penetration.

Our baseline scenario demonstrates the effect of even a relatively small difference in automation penetration. Under our productivity assumptions above, the labor market, on average, must realize a little over 19% of its automation potential to achieve the labor productivity gains in the BLS projections6. Our baseline scenario increases this to 29% of automation potential in the average sector, resulting in a 1.2% annual labor productivity gain from automation economy-wide, by increasing automation penetration in every economic sector by 50%. To demonstrate the effects of this labor productivity change on labor demand in this scenario, we calculate how much employment7 would be needed to produce output at the level of the BLS projection in 2024.

Note that scenario employment is

not a forecast, since increased labor productivity should lead firms to produce more rather than adjust only employment. We will discuss this further in a later section. For the moment, we simply want to get a sense of how many jobs could be automated at a higher rate of automation penetration without any change in output by sector.

Automation and Employment in the Baseline Scenario

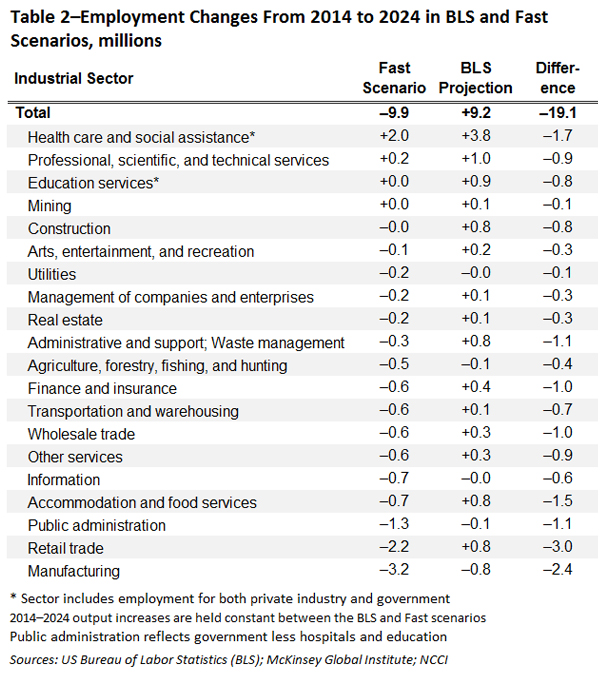

The sectors in Table 1 are sorted by the total change between actual employment in 2014 and the baseline scenario employment in 2024. Naturally, looking at total change in employment combines the effect of increased automation penetration in our scenario with other changes in US demographic and economic factors that change labor demand. We therefore show these two pieces separately as well as combined. The column of the employment change by sector in the original BLS projections represents the benchmark change in employment from all factors—an increase of about 9 million combining all sectors, from 142 million in 2014 to 151 million in 2024. The difference between our baseline scenario and BLS projections, in the third column, represents the reduced employment from that benchmark due specifically to our assumed increase in automation penetration.

Table 1 shows that healthcare and social assistance has the highest employment growth both in the baseline scenario and in the original BLS projections. In fact, healthcare and social assistance adds 3.2 million jobs in the baseline scenario, more than the net employment gain economy-wide. The sector maintains such a high level of employment growth in the baseline scenario because of the large job growth in the BLS projections coupled with low automation penetration. Only 2.5% of healthcare and social assistance workers in the BLS projection could be replaced by automation without losing output in the baseline scenario. The other sectors could combine to achieve projected 2024 total output, a 25% increase from 2014 output, with fewer workers than it employed a decade before.

Other sectors also add or subtract workers in the baseline scenario. Manufacturing would suffer the largest decline by far, 1.6 million, due both to declining employment in the original BLS projections and relatively high exposure to automation penetration. Increased automation penetration in the baseline scenario could replace 6.9% of manufacturing employment on top of manufacturing’s expected employment losses due to import competition and other factors (including a lower level of automation penetration) already present in the BLS projections. Information, agriculture, and retail trade would employ over 200,000 fewer workers in 2024 than 2014, and noneducation government employment would decline as well. In other industries, projected employment growth outweighs losses due to the scenario’s higher automation penetration. The professional services, education, and construction sectors would each need half a million or more jobs to meet output targets even after accounting for faster automation penetration.

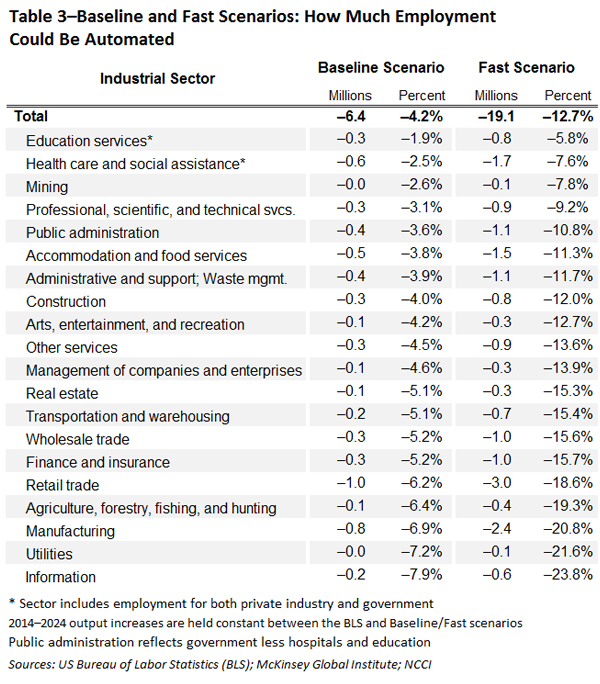

Retail trade would have the biggest job loss directly from increased automation. Automation penetration in the baseline scenario would allow the sector to produce the same amount of output with 1 million fewer workers. Manufacturing, healthcare and social assistance, and accommodation and food services could each employ about half a million fewer workers. Economy-wide, faster automation penetration in the scenario could lower employment by 6.4 million without decreasing output. Here the focus is on levels of employment changes from automation by sector, which combines automation potential and penetration with the size of each industry. This is important for determining where the most people could be affected, but later in this piece, we will discuss potential employment changes by sector in percentage terms as well.

Automation Will Favor Some Job Skills More Than Others

Researchers agree that the most difficult tasks to automate involve creative and interpersonal skills or unpredictable physical tasks, whereas data collection and processing as well as routine physical tasks are more easily automated. This has already led to increasing “job polarization” in the US labor market8, where automation has substituted for many jobs that traditionally fell in the middle of the wage distribution. This includes both physical labor in manufacturing which has been replaced by machines as well as white-collar clerical jobs whose supporting function has been displaced by better software and computing power. The former CEO of Citigroup, Vikram Pandit, said recently in an interview that automation could eliminate 30% of banking jobs in the next five years, warning that in particular, automation is “going to change the back office.”9

At the other end of the spectrum, healthcare and education are large sectors that stand out as difficult to automate. These workers regularly interact with people in an open-ended way and must adapt to student or patient needs, while applying specialized expertise in their subject areas. Healthcare employment will grow over the next decade not only due to low automation potential, but because demographic trends toward population aging increase demand. Over the time period of our projections, the number of Americans over 65 is projected to increase from 45 million to 62 million.10

Jobs Traditionally Held by Women Have Lower Automation Potential

Besides their status as growth sectors, there is another key similarity between the healthcare and education sectors. Both sectors currently employ a high percentage of women. According to the Current Population Survey, 47% of the US labor force is female, but women make up 68% of the workforce in education and 79% in healthcare and social assistance. Men are slowly increasing their representation in traditionally female-dominated professions such as nursing,11 but these trends will have to accelerate to balance the gender ratio among teachers and health service professionals. At the current gender ratio, 3 million of the nearly 4 million new workers needed in these two sectors under the baseline scenario would be women, representing almost all the scenario employment gain in the whole economy. This would exacerbate a worrisome trend of declining labor force participation among young men.

The employment gains and losses by sector are shown in Figure 2, along with the gender composition of these changes at current ratios. This figure does not necessarily mean that men will make up a declining share of the future labor force, but rather illustrates changing labor demand that may cause men to consider different types of work in the near future.

On the other side of the coin, many of the jobs most susceptible to automation are predominantly held by men. The sector with the McKinsey study’s highest automation potential, accommodation and food services, has a roughly balanced gender ratio, but the next-highest automation potentials belong to manufacturing, agriculture, and transportation and warehousing. According to the 2016 Current Population Survey (CPS), men make up between 70% and 80% of the workforce in each of those three sectors.

Even those percentages, which are just as unbalanced toward men as healthcare and education are toward women, may understate gender differences in susceptibility to automation. Our main analysis in this piece is at the sector level, but men are usually concentrated in more automatable jobs within sectors. For example, men make up 76% of transportation and warehousing workers overall, but 89% of workers in truck transportation, a commonly cited target for automation.

Automation and Hazardous Work

Workers compensation rates could potentially decrease in the future as dangerous jobs are automated. This will primarily occur through making work within sectors safer, decreasing frequency of injuries rather than moving workers into sectors with fewer severe hazards. For example, automatic lifts can help make moving hospital patients safer for both patient and staff.12 In addition to reducing hazards within a job by automating repetitive tasks, automation can also reallocate workers in a sector to less hazardous jobs. The McKinsey study uses oil and gas operations as one of its case studies in automation. The study suggests that automation will not reduce total labor in oil and gas occupations much, but simply counting work hours masks an important shift. Automation deployed offshore will reduce dangerous physical labor on rigs, but add more engineering jobs in onshore control rooms.

However, it is far from clear that automation will move people from hazardous occupations into less hazardous occupations. Measured by hazard groups for NCCI classes,13 automation potential does not closely correspond to risk. Manufacturing has high automation potential and its largest classes by payroll are in hazard groups (HG) C and D, while food services and retail trade have high automation potential as well but have low-risk HG A and HG B assignments. Contracting classes are consistently categorized as high hazard, but construction has only average automation potential and the baseline scenario predicts construction employment will increase substantially. Hospital and physician’s office workers have medium-risk HG C assignments, and nursing assistants, in particular, have high rates of back injuries.14

WHAT DRIVES AUTOMATION PENETRATION BESIDES AUTOMATION POTENTIAL?

A variety of economic incentives affect how quickly automation potential translates to actual automation in practice. Automation penetration will depend on the opportunity cost of investment as well as transaction costs in implementing automation.

- Does automation require purchasing and installing new heavy equipment or a software upgrade?

- Are the tasks to be automated currently performed by a skilled machinist making $60,000 a year plus benefits or a couple of part-time cashiers making minimum wage?

- Can new software be deployed internally to reduce overhead or is it part of the core product, which will now face additional government oversight?

The answers to these types of questions can help explain how projected employment effects of automation differ from the effects if automation potential was being realized at equal rates in all industries.

Software or Machinery?

The information sector has the highest expected automation penetration of any sector. This sector, which includes publishing, telecommunications, and data processing and hosting services, covers a wide range of activities. These activities do have one thing in common—automation in these contexts refers to software much more than heavy machinery.

For example:

- Magazine or newspaper layout is done by computers.

- The first line of defense for a problem with your cable is not to schedule a house call, but to have a remote technician sending signals and patches from a centralized control center (or to access your online account and push a button to refresh the signal yourself).

- A computer program can monitor cell signals and automatically reroute traffic in response to error rates or slow traffic. Automation helps designers and technicians in this industry do their jobs more efficiently, and it requires relatively cheap software to implement.

Labor Costs or Capital Investment?

On the other hand, cheaper labor slows incentives to automate. Accommodation and food services has the highest automation potential of any industry but relatively low projected automation penetration. One potential explanation is that food services has a lot of low-wage workers. It may be possible to automate some of these jobs, but when labor is cheap, firms might not think investing in upgrading infrastructure is worth it.

One interesting follow-up question is whether recent initiatives to raise the minimum wage would have an impact on this finding. It certainly makes sense that it could. If workers become more expensive, for example, through a $15 minimum wage as was recently instituted in Seattle, then there is a greater benefit to invest in automation. However, research does not appear to support that minimum wages have a big impact on restaurant employment.15 A recent paper using data from Seattle—which found larger employment effects of the minimum wage than most other studies—found no significant impact on restaurant workers.16

However, it could be these small estimates are short-run effects. Maybe the minimum wage change is not enough to make a fast food restaurant in

Seattle change its staffing behavior, but a minimum wage hike

nationwide would make that restaurant ramp up its investment in self-order kiosks at the corporate level.

Regulation and Political Pressure

Regulation also plays an important role in automation penetration. A common example is self-driving cars. Even when self-driving software reaches the point that it can operate vehicles more safely than humans, and be technically ready for mass production, adoption will have to wait until the technology passes inspection. The US House of Representatives recently passed the SELF DRIVE Act,17 which discusses safety, cybersecurity, and privacy regulations for automated vehicles and driving systems.18

Automation could be slowed by government, not only from regulations produced out of caution, but also from a desire to protect jobs. Staying with the example of automated driving systems, a September Senate hearing shows government’s interest in both the technical and economic impacts of automation. The press release states: “The hearing will examine the benefits of automated truck safety technology as well as the potential impacts on jobs and the economy.”

Bill Gates made headlines in February by floating the idea of taxes related to automation.19 His comments were cited by a city official in San Francisco, who is preparing such a tax proposal in California,20 and in a recent National Bureau of Economic Research working paper, “Should Robots Be Taxed?”21 If automation penetration has large employment effects in the near future, these political considerations may gain steam, much in the same way that outsourcing was a hot-button topic in the 2016 presidential election.

Beyond the Baseline Scenario

Our baseline scenario is, of course, only one possibility among many. We now turn our attention to a few follow-up questions:

- How much do the employment effects in the baseline scenario change at the upper bound of the automation penetration implied by the McKinsey analysis?

- How likely is it that automation will affect the economy primarily through employment levels?

- What other forms could the effects of automation take?

We answer the first question by replicating our calculations in the baseline scenario for a much higher level of automation penetration. We try to gain insight into the other questions by studying historical parallels to automation and current analyses of the nature of the labor market.

Fast Automation Penetration Scenario

Recall that we created the baseline scenario numbers by increasing automation penetration

50% from the values at which our formula match BLS projections. In a high-penetration scenario, we increase automation penetration by

150% instead. This results in a 2.2% labor productivity gain due to automation, in line with the top end of the range estimated by McKinsey.

With this faster rate of automation penetration, the economy could meet output targets with only about 132 million workers, about 10 million fewer than employed today and 19 million fewer than the BLS baseline projection for 2024. Even in this fast scenario, healthcare and social assistance would add over 2 million jobs between 2014–24. Professional services, education, and mining would require slightly more workers, and every other sector’s necessary employment would decline. Manufacturing and retail trade would require 3.2 million and 2.2 million fewer workers in 2024 than in 2014, respectively. Looking at the difference from the 2024 BLS projection rather than 2014 employment, retail trade and manufacturing also see the largest declines due specifically to faster automation penetration. They could meet projected output with 3.0 and 2.4 million fewer workers, respectively. Six additional sectors would require over 1 million fewer workers to produce projected output.

Even the fast scenario—based on the most aggressive automation projections from McKinsey—is small compared with some of the rhetoric surrounding automation. Our scenarios’ employment declines, compared to the BLS benchmark, represent about 4–13% of the projected workforce. Percentage declines roughly half as much as average in education services and twice as much as average in the information sector, which was discussed above as being especially susceptible to labor-displacing software. This is certainly a massive number of people and such job losses would have a major impact on the nation, but it is far more modest than conclusions that half of US jobs are vulnerable22 or Mr. Pandit’s comment that 30% of banking jobs will disappear within five years. The next section discusses reasons that employment changes are likely to be smaller than our scenario projections, and that there is a plausible case that automation won’t affect the path of employment at all—although it will have big effects on the

types of jobs that workers will have in the future.

The main takeaways from the analysis so far include:

- There is an important distinction between technical feasibility of automation and widespread adoption

- Studies estimate that the technical potential exists to automate almost half of US work activities, but for a variety of reasons, adoption will significantly lag automation potential

- In our scenarios, automation could replace 6–19 million workers by 2024 without decreasing output, equivalent to 4–13% of the workforce

Will Automation Eliminate Jobs or Change Them?

The first and simplest reason that employment losses might be lower than in our scenario projections is that both scenarios held output constant. This was intentionally chosen to illustrate how many workers could be replaced by automation, but increased labor productivity in a sector should lower the price and increase the quantity of goods or services demanded. The need to produce more will partially balance the employment displacement from automation.

Some economists strenuously argue against the idea that technological change will cause large-scale unemployment. They draw on examples ranging from the Industrial Revolution to the recent past to demonstrate economic flexibility to create new jobs as progress destroys old ones. Most examples show that when technology replaces labor in a major sector of the economy, other sectors grow to absorb the excess labor. In a few cases, the same technology that substitutes for labor also works to complement labor in the same industry, and jobs are transformed rather than lost.

Historical Examples

The previous issue of the

QEB, showed that agriculture’s share of employment dropped from nearly 40% of US employment in 1900 to 10% in 1950 and less than 2% today, mostly because of tractors and other heavy machinery. However, these millions of workers shifted into other production and services sectors without creating widespread unemployment. Many prominent economists argue that new jobs will replace those lost to automation, just like what occurred after technological destruction of occupations from telephone operators to typists.23

Boston University economist James Bessen highlights a more recent example of a sector-specific innovation: the ATM.24 Seemingly, no technology’s name could be more evocative of technological job displacement than an

automated teller machine. But Bessen shows that bank teller positions surprisingly

increased slightly in the 1980s and 1990s as ATMs were widely adopted. Bessen attributes this to two reasons:

- ATMs lowered the cost of opening a bank branch, so that the number of branches increased

- The job description of a bank teller adapted when much of their routine work was replaced by ATMs

On the second point, Bessen writes, “As banks pushed to increase their market shares, tellers became an important part of the ‘relationship banking team...’ The skills of the teller changed: cash handling became less important and human interaction more important.” This exactly matches the research on future automation: data processing and routine physical tasks are relatively simple to automate. Non-routine tasks and personal interaction are much harder.

Rising Labor Productivity and Reallocating Workers

Despite this kind of success story, most observers agree that productivity gains from automation will usually lower employment in the sectors where that automation takes hold. Even so, increased labor productivity can lead to higher overall employment. David Autor and Anna Salomons make this argument in a 2017 study looking at industry-level data in 19 developed countries since 1970. They write, “Because sectoral productivity growth raises incomes, consumption, and hence aggregate employment ... the negative own-industry employment effect of rising labor productivity is outweighed by positive spillovers to the rest of the economy,” and “We estimate that rapid labor productivity growth in primary and secondary industries has generated a substantial reallocation of workers into tertiary services.”

In less academic language, higher labor productivity creates more jobs than it destroys by increasing overall demand, but the sector becoming more productive needs fewer workers. This has recently meant fewer jobs in sectors like manufacturing and agriculture and more in service sectors like healthcare and accommodation and food services.

Conclusions

Automation will continue to drive important changes in the labor market over the next few years and few decades. While automation may lead to widespread unemployment, the odds are greater that it will

redistribute labor rather than

replace it. This will likely accelerate the long-term shift of employment from production to services, especially in healthcare and social assistance and other fields that involve personal interaction. This change favors female-dominated sectors, and men will have to be willing to consider different career paths than their fathers or be left behind.

Automation also has a strong potential to contribute to income inequality as routine middle-skill jobs continue to be replaced, increasing returns to high-skill professional work complemented by computerization, and moving other workers to low-skill personal services jobs that are slower to automate. Even if the labor market adapts rapidly to create jobs lost to automation, workers will still face massive costs from job turnover, retraining, and stress if half of the time they spend at work today is spent on tasks that may be done by a computer program or a robot before their careers end.

Automation will affect workers compensation more by changing the nature of jobs within industries than by reshuffling the labor force between industries. Automation affects occupations and sectors with low and high compensation rates alike, but in substituting for repetitive tasks, it may lower the rate of workplace accidents and repetitive stress injuries. As in the labor market more broadly, automation’s impact on workers compensation will not happen overnight, with investment and labor costs and regulation slowing automation implementation from maximum feasible levels.

Appendix—Scenario Calculations

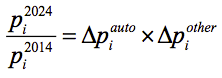

Here we detail how we use the automation potential from the McKinsey study along with BLS projections to create our scenario employment for each sector. Between 2014 and 2024, we assess the percent change in labor productivity

in each sector

i as the product of change in labor productivity due to automation and change in labor productivity due to other factors.

in each sector

i as the product of change in labor productivity due to automation and change in labor productivity due to other factors.

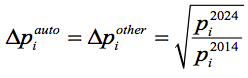

We assume that in the BLS projections, these two elements are the same, and thus:

We relate automation potential, denoted

, and the automation penetration factor, denoted

, and the automation penetration factor, denoted

, to labor productivity using the following formula.

, to labor productivity using the following formula.

The automation potential and automation penetration factor each take on values between zero and one. If either is zero, automation contributes nothing to labor productivity increases over time. As both go to one, labor productivity gain approaches infinity, which implies production with no human employment at all—full automation. For a given level of output and labor productivity gain from non-automation, we can also interpret the product

as the proportion of workers that could be eliminated by automation.

as the proportion of workers that could be eliminated by automation.

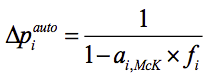

If we use BLS projections for output and employment, we can determine their baseline labor productivity. By combining the assumption that half of BLS labor productivity gain comes from automation with the automation potential from McKinsey, we solve for an implied automation potential in each industry. Then, we multiply each penetration factor

by 1.5 to create our baseline scenario and by 2.5 to create our fast automation penetration scenario.

Finally, we assign automation potential from healthcare and social assistance to government hospital workers and education services to government education workers. We assume a 35% automation potential for other government sectors, similar to professional and management workers.

© Copyright 2017 National Council on Compensation Insurance, Inc. All Rights Reserved.

THE RESEARCH ARTICLES AND CONTENT DISTRIBUTED BY NCCI ARE PROVIDED FOR GENERAL INFORMATIONAL PURPOSES ONLY AND ARE PROVIDED “AS IS.” NCCI DOES NOT GUARANTEE THEIR ACCURACY OR COMPLETENESS NOR DOES NCCI ASSUME ANY LIABILITY THAT MAY RESULT IN YOUR RELIANCE UPON SUCH INFORMATION. NCCI EXPRESSLY DISCLAIMS ANY AND ALL WARRANTIES OF ANY KIND INCLUDING ALL EXPRESS, STATUTORY AND IMPLIED WARRANTIES INCLUDING THE IMPLIED WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE.

Note: Analysis and charts prepared in August and September 2017.