Automation has the potential to transform future jobs and the structure of the labor force. As we discussed in the March edition of the

QEB, automation in manufacturing has steadily decreased costs for decades, making US manufactures more competitive while also reducing the amount of labor required to produce them. Looking forward, technical advances in computing power, artificial intelligence, and robotics have created the potential for automation to penetrate deeply into occupations beyond manufacturing. The prospect that future automation might transform jobs and the labor force on a systemic scale raises some important questions for workers compensation:

- What jobs are more susceptible to automation and what jobs are less susceptible?

- How is the composition of employment across economic sectors likely to change?

- What happens to workers displaced from occupations impacted by automation?

Because of the breadth of this topic, we will present our analysis in two parts. This edition of the

QEB provides historical context for automation and explains why automation in the future has the potential to change labor markets more dramatically than in the past. We review several recent studies that quantify the potential for automation expansion across occupations and economic sectors, and address the question of which jobs are most susceptible to automation. In a follow-up piece to be published later, we will present scenarios for automation penetration across different economic sectors comprising the US economy, from which we will address the questions above concerning changes in the composition of the labor force and what could happen to workers displaced by automation.

AUTOMATION HISTORICALLY

Automation is not a new occurrence, and has contributed to significant shifts in employment throughout the 20th century. With the widespread adoption of the gas-powered tractor in the early 20th century, farmers experienced many benefits including the more efficient use of labor and increased productionI. This contributed to a decline in agricultural employment from close to 40% of total employment in 1900 to less than 2% since 2000, as shown in Figure 1.

Likewise, manufacturing’s share of employment has also declined from a peak of over 25% in the 1950s to less than 10% currently. Much of this decline is due to automation. A Ball State University study found that 87% of the job losses in manufacturing from 2000 to 2010 were due to automation, while 13% were due to globalization and tradeII.

Automation has also contributed to an increase in output, as seen in Figure 2. Since 1990, manufacturing output

grew 71.8% while manufacturing employment

fell 30.7%. This means that in 2016 the United States produced almost 72% more goods than in 1990, but with only about 70% of the workers. Over the same period, US manufacturing labor productivity grew 140.1%III. Automation in manufacturing has decreased production costs, making US manufactures less expensive and more competitive by reducing the amount of labor required to produce them.

Notwithstanding these dramatic impacts, only a small portion of manufacturing tasks are currently automated. By one estimate, only about 10% of manufacturing tasks globally were performed by robots in 2015. But that percentage is expected to rise to 25% by 2025 as robots become less expensive and easier to program, making them more accessible, particularly to small factoriesIV.

AUTOMATION PENETRATION ACROSS SECTORS

Automation is starting to take hold in other sectors beyond manufacturing. Some well-known examples include kiosks and tablets to place orders and pay in restaurants, robots to process packages in warehouses, and self-driving trucks in transportationV.

Until recently, automation displaced routine tasks that were predictable and could be easily programmed. This included assembly line robots in factories and computers to replace certain occupations such as switchboard operators. Today, advances in artificial intelligence and machine learning enable software to detect patterns in data, allowing some nonroutine tasks and judgmental decisions to be automated. Combined with advances in mobile robotics, machine learning can even permit nonroutine manual tasks to be automated—tasks that could only be performed by humans in the past.

Two recent major studies have attempted to identify which tasks are most susceptible to automation with current technology: "A Future That Works: Automation, Employment and Productivity," by the McKinsey Global InstituteVI; and "The Future of Employment: How Susceptible Are Jobs to Computerisation?" by Carl Frey and Michael Osborne at the University of OxfordVII. We discuss the findings of these studies in the following two sections. Subsequent sections contain a brief survey of related studies by other authors, and a discussion of how the labor market impacts envisioned by recent research on automation differs from more conventional labor market forecasts, such as those published by the US Bureau of Labor Statistics.

MCKINSEY STUDY

Using data from the US Department of Labor for 800 occupations, the McKinsey study identified 2,000 distinct work activities. Each work activity requires some combination of 18 performance capabilities, which come from five groups: sensory perception, cognitive capabilities, natural language processing, social and emotional capabilities, and physical capabilities. For each occupation and activity, McKinsey determined which performance capabilities are demanded, and whether the required level of performance is below, at, or above a median level of human performance. McKinsey then rated the potential for existing technology to substitute for humans in each performance capability in each occupation and activity.

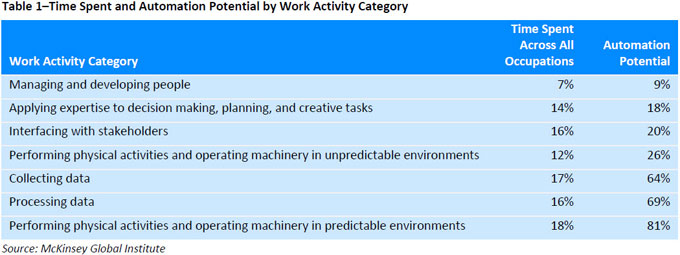

Finally, McKinsey aggregated its 2,000 work activities into seven broad categories. Table 1 shows the average percentage of time spent on each activity category across all occupations, as well as its potential for automation. For example, a 69% automation potential for processing data means that over two-thirds of the time currently spent on this activity by human workers across all occupations might be saved by automation with existing technology.

McKinsey estimates that only 7% of time is spent managing and developing people, and that this is the work activity with the lowest automation potential of 9%. The next three work activities—applying expertise, interfacing, and performing unpredictable physical activities—make up 42% of time, with automation potentials ranging from 18% to 26%. The three remaining categories—collecting data, processing data, and performing predictable physical activities—comprise 51% of all work activities and have high automation potentials ranging from 64% to 81%.

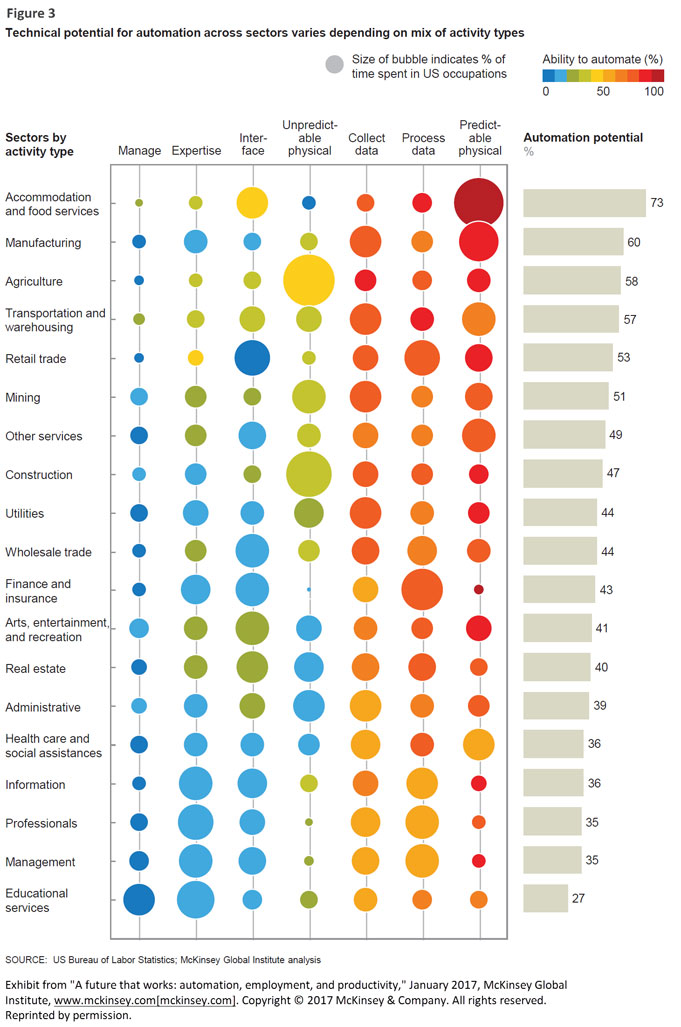

Figure 3 presents McKinsey’s estimates of automation potential by economic sector. Automation potential in an economic sector depends on the shares of time spent on the different work activity categories from Table 1. Circle sizes indicate the amounts of time spent on each work activity, while their colors indicate the automation potential for that activity in the indicated sector. The bar at the right indicates the overall automation potential for the associated sector.

With automation potential of 73%, accommodation and food services is the sector most susceptible to automation with existing technology. A large percentage of work time in this sector is spent on predictable physical activities, the activity category with highest automation potential. Manufacturing and agriculture rank next highest, suggesting that historical automation trends in these sectors are likely to continue. Least susceptible to automation are jobs relating to healthcare, information, professional and management services, and education. These jobs demand higher shares of time spent on managing and developing people and applying expertise to decision making, the two activity categories with the lowest automation potential.

McKinsey’s estimates indicate that the potential for workplace automation depends on the type of occupation. While fewer than 5% of all occupations might be fully automated, about 60% of occupations could have at least 30% of their activities automated. In McKinsey’s baseline scenario, 49% of all of today’s work activities may be automated using currently available technology by 2055. However, McKinsey throws a wide confidence band around this timeline by suggesting that the same degree of automation penetration might occur 20 years earlier in 2035, or 20 years later in 2075. Clearly, estimating the technical potential for automation is one thing, but estimating the speed with which automation occurs is another. McKinsey notes that numerous factors are likely to impact the timing and extent of automation penetration in different occupations, including technical complications in specific job applications, capital investment necessary to develop and deploy solutions, labor costs including benefits and liabilities, and regulatory and social acceptance.

OXFORD STUDY

The Oxford study is based on descriptions of specific tasks for 702 different occupations from the US Department of Labor. Using these descriptions and working with machine learning experts, authors Frey and Osborne identified 70 occupations that they consider to be either entirely automatable or entirely nonautomatable. In doing so, they considered the degree to which each occupation requires any of three bottlenecks to automation: perception and manipulation, creative intelligence, and social intelligence. Perception and manipulation includes finger dexterity, manual dexterity, and awkward positions; creative intelligence includes originality and fine arts; and social intelligence includes social perceptiveness, negotiation, persuasion, and assisting and caring for others. Finally, using these 70 occupations as a basis, Frey and Osborne applied a classification algorithm to assign a degree of automation potential between zero and one to each of the remaining 632 occupations.

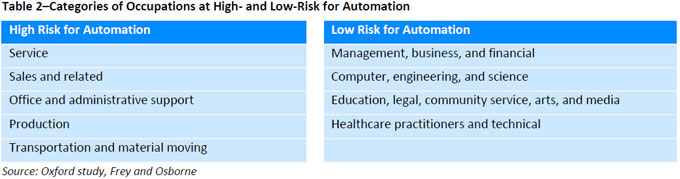

Their results suggest that 47% of total US employment is in occupations at high risk for automation (probabilities greater than 70%), while 19% of employment is in occupations at medium risk (probabilities between 30% and 70%), and 33% of employment is in occupations at low risk for automation (probabilities less than 30%). Categories of occupations comprising the highest shares of employment in high- and low-risk automation groups are listed in Table 2.

Although they use different approaches, the Oxford and McKinsey studies reach similar conclusions. Occupations with higher (or lower) automation risk in the Oxford study are exactly those that are typical in the economic sectors identified by the McKinsey study as having similar degrees of automation risk. Economy-wide estimates of automation potential are also similar for both studies: the McKinsey study estimates that 49% of today’s work activities could be automated with currently available technology; the Oxford study concludes that 47% of US employment is in occupations at high risk for automation.

Like the McKinsey study, the Oxford study makes no definite predictions about a timeline for automation, but emphasizes that the speed of automation in various occupations will depend on a variety of factors. Among these, the Oxford study points to the difficulty of overcoming automation bottlenecks like perception and social intelligence, resistance from stakeholders, and the level of wages relative to the cost of automation. Both studies conclude that industries or occupations with a higher potential for automation are likely to be impacted sooner than those with lower potential.

ADDITIONAL STUDIES

This section contains a survey of additional research on automation, some of which extends results from the McKinsey and Oxford studies.

-

Citigroup.VIII The Citigroup study extends the Oxford estimates both globally and regionally.

- Using World Bank data for over 50 countries, Citigroup found that the average share of employment at high risk for automation across Organization for Economic Cooperation and Development (OECD) countries is 57%, with shares as high as 69% in India and 77% in China.

- Citigroup also estimates the share of employment at high risk of automation for US cities:

- Fresno, CA and Las Vegas, NV had the highest shares of employment at risk of automation, 53.8% and 49.1%, respectively. Cities at high automation risk tend to specialize in industries such as services, sales, office support, and manufacturing. These also tend to be cities with lower wages.

- Boston, MA and Washington, DC had the lowest employment shares at risk of automation, 38.4% for both. Cities at lower risk generally have more diversified labor forces and more skilled workers in technological industries.

-

University of Redlands.IX The University of Redlands study combines the Oxford study’s estimates with employment data to identify US metropolitan areas most susceptible to automation.

- Most US metropolitan areas are at risk of losing over 55% of their current jobs due to automation.

- Metropolitan areas Las Vegas, NV; El Paso TX; and Riverside-San Bernardino, CA have more than 63% of their jobs at risk of automation. These areas have concentrations of lower wage jobs relating to office support, food preparation and serving, sales, and transportation and material moving.

- High-tech metropolitan areas such as Boston and Silicon Valley have fewer jobs at risk.

-

OECD.X This study evaluates the potential for automation for 21 OECD countries. It argues that the McKinsey and Oxford studies may overstate the number of workers at risk from automation for several reasons:

- First, the OECD stresses the importance of economic, legal, or societal factors that may inhibit the adoption of new technologies.

- Where the cost of the new technology exceeds the cost of labor, adoption will be slower.

- Legal questions may slow technology adoption: for example, assigning liability in accidents with a driverless car.

- People may prefer that certain tasks be performed by humans instead of machines, like nursing.

- Second, the OECD considers what might happen to human workers in a more automated workplace.

- As new technology is adopted, workers may switch within their workplaces to more complex tasks that cannot be automated, such as programming and monitoring.

- New technology related to automation may create jobs or raise wages.

- Job creation related to production and service of automation tools and technologies.

- By reducing production costs, automation will lead to higher output in affected industries, ameliorating the displacement effect on workers.

- Automation which increases worker productivity may also increase wages.

DEPARTURE FROM CONVENTIONAL LABOR FORCE FORECASTS

While subject to a lot of conjecture and uncertainty, the McKinsey and Oxford studies point to magnitudes of feasible job automation that go far beyond conventional forecasts for future output and employment in the US economy. Conventional forecasts, like those from the US Bureau of Labor Statistics (BLS) or Moody’s Analytics, are typically based on econometric models that extrapolate historical labor productivity trends into the future. In contrast, the McKinsey and Oxford studies suggest that automation penetration could accelerate dramatically in many economic sectors, with the consequence that labor productivity in those sectors would also jump relative to historical trends.

For example, the most recent output and employment forecast from the BLS projects a cumulative labor productivity gain from 2017 to 2024 of 12% for the US economy excluding government. Over the same period, if automation were to substitute for BLS’s estimate of new jobs at McKinsey’s 49% estimate, then US labor productivity would instead increase 14%.

Similarly, the BLS’s output and employment forecast indicates cumulative productivity gains over the same period of 7% in healthcare and social assistance, and 11% in construction—two sectors with high rates of projected employment growth. If we apply McKinsey’s estimates for technically feasible automation in these sectors to substitute for labor in the BLS’s estimates of new job creation, then the labor productivity gain in healthcare and social assistance would increase to 12%, and in construction to 16%. More automation means that workers in these sectors could become substantially more productive, but also that fewer workers would then be needed to produce a given amount of output or services.

WHAT MIGHT AUTOMATION MEAN FOR THE FUTURE LABOR MARKET?

In a follow-up piece to this

QEB, we will present scenarios for automation penetration across economic sectors of interest to workers compensation, which collectively comprise most covered employment in the US. Using McKinsey’s estimates for potential automation penetration in different economic sectors, we will address the following questions at the national level:

- What happens to workers in economic sectors impacted by automation?

- In an industry or sector, automation increases worker productivity, which means that the same amount of output could be produced with fewer workers. However, more productive workers also earn higher wages, and lower production costs mean lower prices and more output demanded, which tends to raise employment. Total employment in a sector will depend on the interplay of these effects.

- How might the distribution of employment across economic sectors change as the result of automation?

- In the national economy, employment shares can be expected to shift from sectors more impacted by automation to other sectors that are less impacted. How might re-equilibration in the labor market affect the overall size of the labor force and the employment shares of different industries and occupations?

FORTHCOMING RESEARCH: SCENARIOS FOR AUTOMATION AND THE FUTURE LABOR MARKET

A follow-up piece will present scenarios for the potential impact of automation on the US labor market, addressing what might happen to workers in economic sectors impacted by automation, and how the distribution of employment across economic sectors may change as a result of automation.

© Copyright 2017 National Council on Compensation Insurance, Inc. All Rights Reserved.

THE RESEARCH ARTICLES AND CONTENT DISTRIBUTED BY NCCI ARE PROVIDED FOR GENERAL INFORMATIONAL PURPOSES ONLY AND ARE PROVIDED “AS IS.” NCCI DOES NOT GUARANTEE THEIR ACCURACY OR COMPLETENESS NOR DOES NCCI ASSUME ANY LIABILITY THAT MAY RESULT IN YOUR RELIANCE UPON SUCH INFORMATION. NCCI EXPRESSLY DISCLAIMS ANY AND ALL WARRANTIES OF ANY KIND INCLUDING ALL EXPRESS, STATUTORY AND IMPLIED WARRANTIES INCLUDING THE IMPLIED WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE.

Note: Analysis and charts prepared in May and June 2017.