Like a safe-driving discount, employers with good safety records can save on workers compensation insurance premiums. But how strong is the connection between past loss history and future losses? As NCCI continues its review of Experience Rating Plan performance, answers to that question and confirmation of plan performance are becoming clearer.

For many insureds, experience rating plays an important role in determining their workers compensation premiums. If an insured meets the premium eligibility requirements, experience rating adjusts its future premium based on its past loss experience. Insureds with fewer past losses than anticipated by the approved manual rates will receive an experience rating modification that lowers their future premium, and vice versa. The NCCI experience rating modification (the “Mod”) promotes pricing equity, loss prevention, and timely return to work.

In 2017, NCCI started a multiyear project to both comprehensively review the performance of its Experience Rating Plan (the Plan), as well as test various plan alternatives.

Key findings from this ongoing review shared at NCCI’s

Annual Issues Symposium (AIS) 2019 include:

- For all states combined, the Plan performs well

- Plan performance varies by industry group

- A longer claim history (more than the three years typically used in experience rating) improves the Mod’s ability to predict future loss ratios, especially for smaller insureds

- “Scaling up” (described later) medical-only losses makes the Mod more predictive

Findings discussed in this article should not be interpreted in any manner as potential structural changes to NCCI’s Plan. NCCI’s experience rating research is ongoing and no changes to the Plan, if any, will be considered until the review is completed.

BACKGROUND

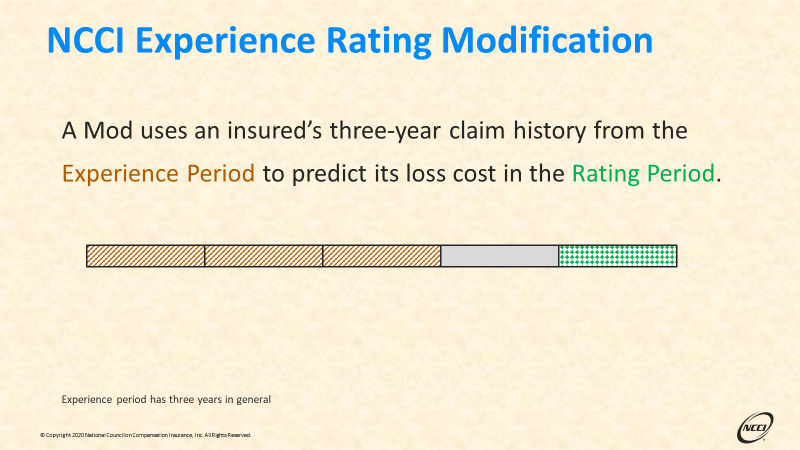

Experience rating uses an insured’s losses in a three-year experience period to calculate the Mod and predict the insured’s ultimate unlimited losses in the rating period (i.e., the prospective policy period). For example, loss experience from the three-year period 7/1/17 to 7/1/20 would generally be used to determine the Mod for a policy effective 7/1/21.

Exhibit 1

To test Plan performance, NCCI compares the Mod, calculated based on the actual and expected losses during the experience period, with the loss ratio incurred during the rating period. NCCI evaluates Plan performance in two dimensions: (1) predictive power and (2) calibration accuracy. Following are the performance test steps:

- Sort insureds into five groups, or quintiles, in ascending order by Mod.

- Review the loss ratios from the rating period—using the ratios of actual to expected losses

before the Mods have been applied—to assess the Mod’s predictive power.

- Review the modified loss ratios from the rating period—using the ratios of actual to expected losses

after the Mods have been applied—to assess the Mod’s calibration accuracy. “Modified expected losses” result after multiplying expected losses by the Mod and serve as an estimate of the insured’s future premium.

If the Mod is predictive of future loss ratios, significant differences in loss ratios would be expected across the quintiles before applying the Mod. If the Mod is accurate, which means the appropriate debits and credits are being applied to the expected losses, the loss ratios would be expected to be flat across the quintiles after applying the Mod.

FINDINGS

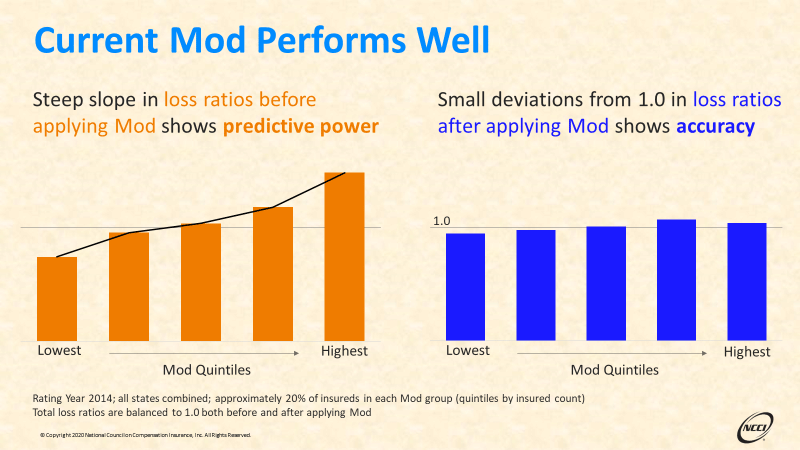

For all states combined, the Plan performs well, showing both great predictive power and calibration accuracy.

1.

Predictive power—shown in the rating period loss ratios before applying the Mod

- The orange bars on the left in Exhibit 2 show that the rating period actual loss ratios increase monotonically and exhibit significant differences across quintiles, indicating that the Mod has great predictive power.

- The predictive power, measured as the difference in loss ratios—prior to the Mod—between the highest and the lowest quintiles, is 0.74 in this case. While this is a popular approach for measuring predictive power, it has limitations—it ignores all quintiles other than the highest and the lowest, and therefore can be incomplete and volatile.

2.

Calibration accuracy—shown in the rating period loss ratios after applying the Mod

- The blue bars on the right in Exhibit 2 show that the modified loss ratios across quintiles are close to 1.0, indicating the Mod has good calibration accuracy overall; that is, within each quintile, the average modified expected losses are close to the actual losses.

- Looking closely at the blue bars, some small deviations are apparent: the first quintile is slightly below 1.0, while the last two quintiles are slightly above. These departures from unity indicate that there may be opportunities to further refine the Mod’s accuracy.

Exhibit 2

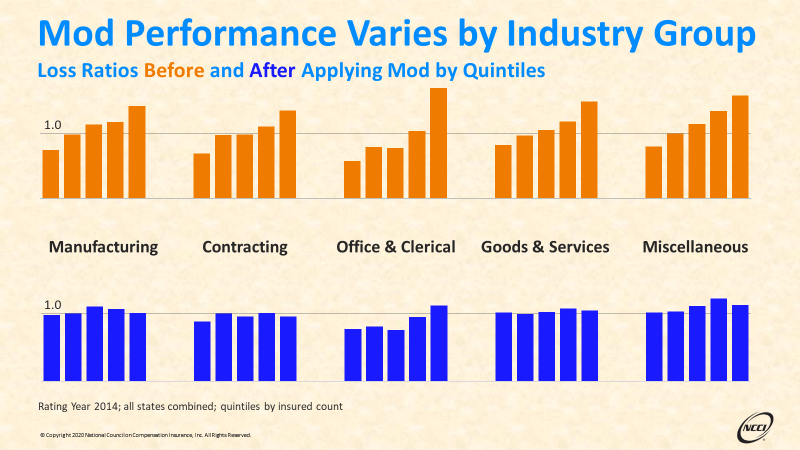

Plan performance varies by industry group.

NCCI categorizes insureds into five industry groups based on the group in which the insured has the largest volume of expected losses. Manufacturing is 18%, Contracting is 22%, Office & Clerical is 9%, Goods & Services is 32%, and Miscellaneous is 19% of the expected losses in the data used for this analysis.

Exhibit 3

Overall, the Plan performs well across all industry groups—indicative through solid predictive power in loss ratios before applying the Mod, and relatively flat loss ratios after applying the Mod (Exhibit 3). However, one industry group that stands out is

Office & Clerical. It has the greatest predictive power before the Mod (as shown by the orange bars at the top), yet also shows the most noticeable departures from 1.0 after the Mod (as shown by the blue bars at the bottom). NCCI is looking into the causes of the performance differences. We are also looking into ways to further improve the Plan’s accuracy by industry group or possibly a more granular level. Improving performance in this area is a focus of our current review.

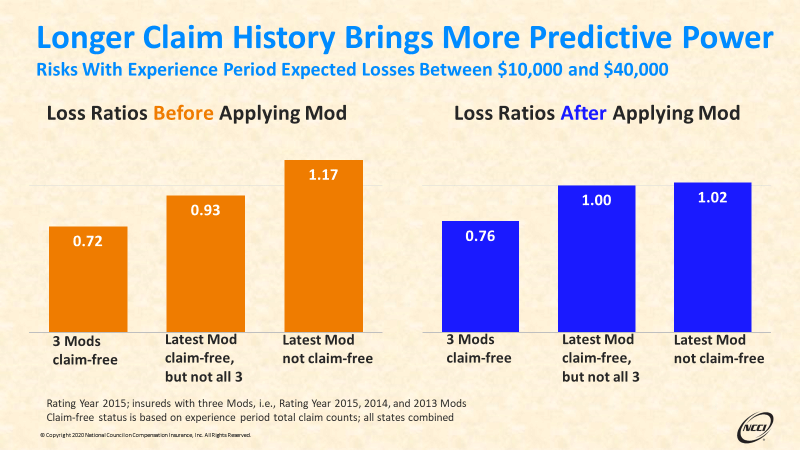

A longer claim history brings more predictive power.

In general, Mods are calculated using a three-year claim history. Would more years of history improve the Mod’s predictive power? To address this question, insureds were categorized based on whether they had claims in one or more of the experience periods used in the three most recent Mod calculations. More specifically, the three categories were:

1. Insureds that were claim-free in all three Mod experience periods; this is roughly equivalent to insureds that were claim-free for five years

2. Insureds that were claim-free in the experience period for the most recent Mod, but were not claim-free for the previous two Mods; this is roughly equivalent to insureds that were claim-free for three years but not five years

3. Insureds that were not claim-free in the experience period for the most recent Mod

Exhibit 4

Focusing on the blue bars on the right in Exhibit 4, if a longer claim history brings more predictive power, a difference in the modified loss ratios between the first and second categories would be expected. There is indeed a material difference in the modified loss ratios between the first two blue categories (0.76 versus 1.00). This indicates that the insureds in the first blue group, that have not experienced a claim over the most recent five years, have a lower loss ratio than those that have only been claim-free over the most recent three-year period—even after applying the Mod.

A longer claim history gives more predictive power with respect to differentiating those two groups of insureds. Large insureds are rarely claim-free. Once an insured is large enough, it is expected to have claims; therefore, this analysis of claim-free insureds is mostly applicable to smaller insureds. One critical practical issue with the use of longer experience periods is tracking ownership changes across multiple rating periods; today this can be challenging with three years of experience. This will be addressed later in our current review.

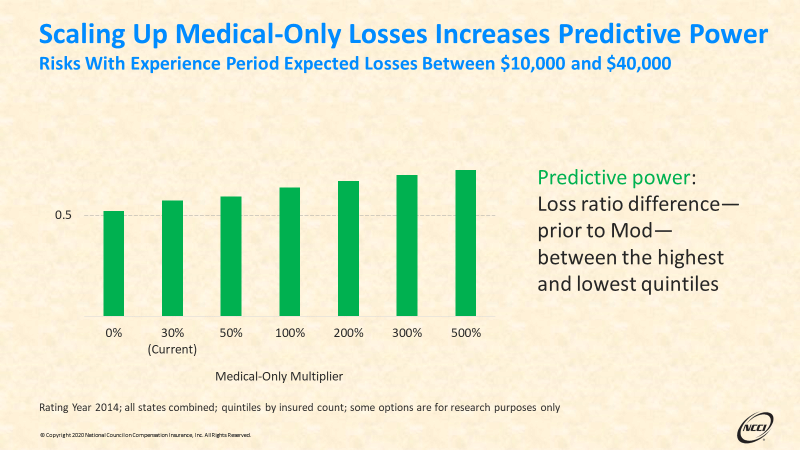

Scaling up medical-only losses in the current Mod calculation increases predictive power.

In 1998, NCCI instituted the Experience Rating Adjustment (ERA) to address the concern that medical-only claims were being underreported. This adjustment lessens the impact on the mod from these small claims and minimizes the financial incentive to the employer to pay these claims out of pocket (and not report these claims to the insurer). All NCCI states except for two are subject to the ERA, where only 30% of the actual primary and excess portions of each medical-only loss are included in the Mod calculation. As an interesting exploration, we applied multipliers ranging from 0% to 500% to medical-only losses to see how the Mod’s predictive power changes. Note that this exploration was done for research purposes only. At the present time, NCCI does not have any plans to use multipliers of medical-only losses that are larger than 100% in the actual Mod calculation. The theoretical advantage in predictive power in doing so is unlikely to be realized due to the potential growth in underreporting of these claims.

Exhibit 5

Each bar in Exhibit 5 shows the predictive power of the Mod using the medical-only multiplier shown below the bar. For small insureds—those with experience-period expected losses between $10,000 and $40,000—the Mod’s predictive power increases as a multiplier greater than the 30% used in the current Plan is applied.

Compared with lost-time claims, medical-only claims have much less of an impact on the Mod because they are much smaller. As a result, the claim frequency information captured by medical-only claims, which is predictive of an insured’s future losses (especially for small insureds), is muted and not fully utilized in the current Plan. Amplifying the medical-only losses allows the Mod formula to leverage more of that frequency information. When the same analysis is done on larger insureds, the gain in predictive power is still present but less significant. In addition, for the largest group of insureds in our study, the increase in predictive power hits a turning point as the multiplier exceeds a value between 100% and 200%.

SUMMARY OF KEY FINDINGS

The most recent Experience Rating Plan review shows that the Plan performs well for all states combined, having both great predictive power and calibration accuracy. However, there may be some potential opportunities for improvement:

- Mild deviations from 1.0 in the modified loss ratios by quintile suggest that the Plan’s accuracy may be improved

- The Office & Clerical industry group still shows noticeable deviations from 1.0 in its modified loss ratios

- Extending claim history to more than the three years typically used could further improve the Mod’s predictive power, especially for smaller insureds

- Scaling up medical-only losses in the current Mod calculation increases the Mod’s predictive power, highlighting the need to leverage more claim frequency information for smaller insureds

Plan performance is an area of ongoing research at NCCI. This article summarizes the findings shared at NCCI’s

AIS 2019. Some of our findings are guiding structural decisions on future Plan revisions. Other findings are not practical to implement on an industrywide basis, but nonetheless, can provide useful insights. NCCI’s experience rating research is ongoing, and we will continue to keep stakeholders updated. In future articles, we will delve more deeply into the study of the potential opportunities, discerning whether they reflect the need for any adjustments to the Plan.

This article is provided solely as a reference tool to be used for informational purposes only. The information in this article shall not be construed or interpreted as providing legal or any other advice. Use of this article for any purpose other than as set forth herein is strictly prohibited.