Introduction

Every year, NCCI analyzes the overall adequacy of loss plus loss adjustment expense (LAE) reserves held by private carriers in the workers compensation (WC) insurance industry.1,2 The results reflect a comparison of projected ultimate loss ratios from NCCI’s analysis (NCCI selections) with those reported by carriers.3,4 NCCI’s loss reserve analysis helps monitor the health of the WC industry. After its actuarial review, NCCI analyzes changes in reserve-setting practices or other changes which may impact the WC industry.

This article discusses NCCI’s annual loss reserve analysis. Analyzing loss ratios and the industry’s overall reserve adequacy is key to understanding the underlying drivers of the WC industry’s results. The results of this year’s analysis are consistent with those observed in the recent past:

- Reserve levels remain strong

- NCCI-projected industry loss and LAE ratios continue to be below those reported by carriers

Loss Reserve Analysis—Components

While it is possible that pandemic-related conservatism may have somewhat impacted the carrier-reported 2020 loss ratios, the COVID-19 pandemic has not had a major direct or indirect impact on the WC industry loss reserve analysis to date. Even so, NCCI observed a decrease in net earned premium5 volume between Calendar Years 2019 and 2020—partially attributable to COVID-19-related payroll declines.

Overall Reserve Adequacy

For a given year-end date, an overall reserve

redundancy results when NCCI’s selected reserves, summed over all accident years (AY), are lower than total carrier-reported reserves (i.e., a negative number, represented by blue bars in the chart below). Conversely, a

deficiency is indicated when NCCI’s selected reserves are higher than carrier-reported reserves.

This chart highlights the cyclical nature of historical industry results and alternating periods of increasing and decreasing levels of overall reserve adequacy. NCCI’s three most recent year-end analyses have shown industry reserve redundancies—with the year-end 2020 estimate at $14B (approximately 12% of reported reserves). Almost one-third ($4B) of this redundancy is attributable to AY 2020—with nearly all of the remaining redundancy associated with AYs 2011 through 2019.

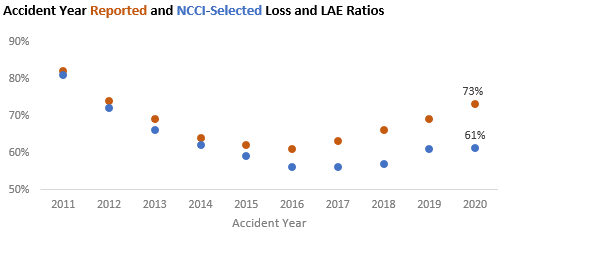

Loss and LAE Ratios

The chart below displays carrier-reported and NCCI-selected loss and LAE ratios valued as of year-end 2020 and shows the following:

- NCCI’s industry loss and LAE ratios selections (in blue) are less than 65% for each of the most recent seven accident years, 2014 through 2020.

- A generally increasing trend—that is, a relative rise in industry loss ratios—since 2016 is apparent, as shown by the higher blue and orange circles as one moves from left to right beginning in 2016.

- For each of the accident years shown, the carrier-reported loss and LAE ratios (in orange) are higher than NCCI’s selections—and the gap between the two has generally widened since 2015.

- Given the uncertainty surrounding the COVID-19 pandemic, NCCI’s selected AY 2020 loss and LAE ratio reflects a relatively higher degree of conservatism within the range of reasonable estimates when compared with that for the more mature years shown. A higher level of conservatism may also be a contributing factor to the relatively higher AY 2020 carrier-reported loss and LAE ratio.

The chart below shows how the carrier-reported loss and LAE ratios have matured over time. The ratio for each year, as initially reported, is at the top in lighter orange. The year’s corresponding darker orange circle is the carrier-reported loss and LAE ratio as of year-end 2020. The gray circles in the chart represent the carrier-reported loss and LAE ratios at each intermediate year-end date (from light to dark). They highlight how the loss and LAE ratios for each accident year have decreased over time.

In general, the loss and LAE ratios shown have declined over time as the year has matured. For example, the carrier-reported loss and LAE ratio for AY 2015 was initially 72% as of year-end 2015. As of year-end 2020, it is 62%. This represents a 10-percentage point decrease as that year has matured. Going forward, NCCI expects the carrier-reported loss and LAE ratios for the more recent (i.e., less mature) AYs to decrease and move closer to NCCI’s selections.

Underlying Drivers of Results

In addition to reviewing the results of the industry loss reserve analysis, it is critical to also examine the underlying drivers of the results. Changes in the industry’s reserve adequacy and differences between carrier-reported and NCCI’s selected loss and LAE ratios may reflect the combined impact of several factors, including:

- The insurance underwriting cycle

- Carrier differences in reserve-setting practices

- Potential conservatism within the range of reasonable estimates in setting reserves for long-tailed lines, such as WC

- Uncertainty around items such as future medical inflation, and the direct and indirect impacts of the COVID-19 pandemic

Insurance Underwriting Cycle

Upward and downward trends in loss and LAE ratios may be part of the insurance underwriting cycle. The chart below illustrates this by providing historical carrier-reported loss and LAE ratios. Periods of increasing ratios are in blue, while periods of declining ratios are in orange. A combination of factors influences the increasing and decreasing patterns in the chart.

Declining claim frequency heavily influenced the period of declining ratios between 2011 and 2016, for example. However, loss and LAE ratios increased year-over-year between 2017 and 2020 despite favorable emergence patterns and continued decreases in claim frequency. Changes during this period may reflect increasing competition for WC where charged premiums declined more rapidly than the corresponding decline in carriers’ losses and LAE.

It remains to be seen if recent changes in premium, underwriting focus, loss improvement, or other factors will serve to reduce the going-forward magnitude of WC underwriting cycle peaks and valleys relative to those observed in the past.

Conclusion

As a result of NCCI’s most recent loss reserve review, it is expected that current carrier-reported loss and LAE ratios will generally continue to decline as the individual AYs mature. NCCI will continue to annually review the adequacy of the WC industry’s loss and LAE reserves and share our findings with interested stakeholders.

This article is provided solely as a reference tool to be used for informational purposes only. The information in this article shall not be construed or interpreted as providing legal or any other advice. Use of this article for any purpose other than as set forth herein is strictly prohibited.