At its

Annual Insights Symposium (AIS) in May 2023, NCCI presented the

State of the Line Report—a comprehensive account of financial results for the workers compensation (WC) insurance line of business. The results presented in that report reflected the most current data available at the time, including NCCI’s preliminary estimates for Calendar Year 2022. In this report, NCCI provides updated results for 2022, as well as preliminary information for 2023.

Key Takeaways

The final countrywide analysis shows that:

- WC Calendar Year 2022 private carrier net written premium (NWP) increased from 2021 by 11.3% to $42.5 billion

- The WC Calendar Year 2022 private carrier combined ratio was 84.0%, and the operating gain was 24.6%

While still early and subject to revision, preliminary analysis through the second quarter of 2023 shows that:

- WC Calendar Year 2023 private carrier direct written premium (DWP) increased 5% through the first half of 2023, compared with DWP through the first half of 2022

- The WC Calendar Year 2023 private carrier direct loss ratio through the first half of 2023 is at 47%, the same as that observed through the first half of 2022

Final WC Results for 2022

For Calendar Year 2022, the most recently reported (as of May 27) WC written premium volume net of reinsurance (NWP) is $42.5 billion for private carriers. This is unchanged from the NWP estimate presented at

AIS 2023 and represents an 11.3% increase from 2021’s NWP volume of $38.2 billion. Including state funds, the Calendar Year 2022 NWP volume is $47.5 billion.

For the Calendar Year 2022 WC net combined ratio for private carriers, updated industry data indicates no change from the previously estimated 84.0% presented at

AIS 2023. This represents a 16.0% underwriting gain. For state funds, the Calendar Year 2022 WC net combined ratio is 115%, resulting in an 87.2% net combined ratio for the total WC industry.

The Calendar Year 2022 combined ratio is the second lowest combined ratio in recent history marking the sixth consecutive year under 90% and the ninth consecutive underwriting gain for the WC industry. The current period of consecutive underwriting gains is unprecedented in terms of both duration and magnitude, resulting in a prolonged soft market atypical of the underwriting cycle.

The WC investment gain on insurance transactions (IGIT) measures investment performance by comparing investment income allocated to the WC line of business with the corresponding earned premium. At

AIS 2023, the IGIT for Calendar Year 2022 was estimated to be 9% of net earned premium. Updated industry data indicates a ratio of 8.6%, which is below the long-term average.

The WC pretax operating gain measures the overall financial performance of the WC line of business, reflecting both underwriting and investment income. The Calendar Year 2022 underwriting gain of 16.0%, combined with the investment gain of 8.6%, resulted in a WC operating gain of 24.6%. This value is slightly lower than the preliminary estimate of 25% shared at

AIS 2023 and marks the sixth consecutive operating gain exceeding 20% for the WC industry.

Preliminary 2023 Analysis

For preliminary 2023 analysis of WC financial results, NCCI uses NAIC Quarterly Statement data. It is important to note that data on a direct basis is available quarterly, while data on a net basis is only available annually—thus, our initial observations for the first half of 2023 rely on the quarterly information available on a direct basis.

Countrywide, NAIC private carrier DWP increased 5.0% through the first half of 2023, compared with DWP through the first half of 2022. The table below summarizes the cumulative DWP changes through the first and second quarters of 2023, compared with the same time periods in 2022.

In contrast to the large DWP growth of +10.6% experienced in Calendar Year 2022, the DWP change of +5.0% observed through Second Quarter 2023 is more moderate. Since premium is calculated as payroll times rate, the impact of combined changes in each component (payroll and rates), generally comprise the overall change observed in premium. However, changes in other factors also contribute to the total premium change such as changes in schedule rating, dividends, rate/loss cost departure, average experience mod, deductible credit types or amounts, and/or the mix of policy types.

Premium decreased significantly in 2020 driven by payroll declines because of the COVID-19-related economic recession; premium then increased slightly in 2021 followed by a full rebound in 2022. The rebound in 2022 premium surpassed the pre-pandemic premium volume and was significantly influenced by both strong employment levels and wage increases. For 2023, payroll growth has slowed due to cooling wage growth. Payroll for the first half of 2023 increased by 7% compared to a nearly 10% increase in 2022 relative to 2021 (source: US Bureau of Labor Statistics).

While payroll changes in recent years have generated upward growth in premium, recent changes in rates/loss costs have provided an offsetting impact. NCCI expects the impact of rate/loss cost level changes on premium to decrease in 2023 by 7.6%, on average, as a result of recent rate/loss cost filings made in jurisdictions where NCCI provides ratemaking services. The changes shown below reflect both voluntary and assigned risk market approvals.

Decreases in bureau rate/loss costs across several recent years are driven by improved experience. Claim frequency continues to follow a long-term pattern of decline, while severity has been moderate and generally offset by wage inflation. Looking at trends in the overall loss ratios (i.e., losses relative to premiums), which considers the combined impacts of frequency and severity net of wage inflation, the result is a declining trend.

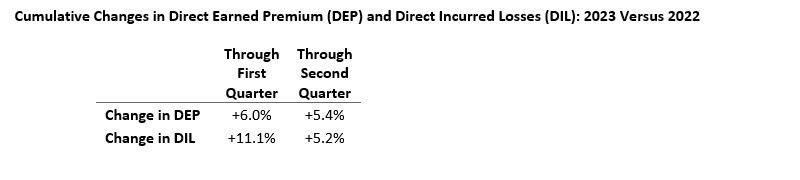

To understand the profitability of the WC line, NCCI reviews the results of the countrywide combined ratio. The largest component of the combined ratio is the loss ratio, which is calculated as the sum of losses divided by premium. The table below summarizes the cumulative changes in countrywide private carrier direct earned premium (DEP) and direct incurred losses (DIL) through the first and second quarters of 2023, compared with the respective time periods in 2022. DEP increased 5.4% through the first half of 2023 compared with the first half of 2022, and DIL increased 5.2% over this same time period.

This results in a direct loss ratio of 47% for the first half of 2023, which is virtually unchanged from the direct loss ratio observed through the first half of 2022. By the end of 2022, the loss ratio developed downward to 43%. This pattern, where the loss ratio develops downward from the first half to the end of the year, has been consistent for eight of the past 10 years. Therefore, it is reasonable to expect that the 2023 loss ratio will develop similarly.

Since NAIC Quarterly Statement data does not include net of reinsurance information, NCCI makes the following assumptions to estimate year-end 2023 WC net values:

- The development of DWP, DEP, and DIL from Second Quarter 2023 to a year-end value is similar to the development observed in recent years.

- The changes in NWP, NEP, and NIL compared to changes in DWP, DEP, and DIL, respectively, follow a consistent ratio with that observed in recent years.

In addition, because quarterly NAIC data does not contain expenses by line of business, NCCI assumes that WC expense ratios for 2023 will be equal to a five-year average, excluding the highest and lowest values, of the expense ratios from Calendar Years 2018 through 2022. Note that expense ratios do not change significantly from year-to-year.

With these assumptions in place, it is reasonable to expect that the countrywide WC Calendar Year 2023 private carrier NWP total will be larger than the $42.5 billion figure observed for 2022. Moreover, given that NCCI estimates the 2023 loss ratio to be similar to that of 2022—coupled with no change from 2022 in the expense component—it is reasonable to expect that the countrywide WC Calendar Year 2023 private carrier combined ratio will also be very similar to 2022. This would result in a full decade of WC calendar year combined ratios under 100%.

Our full year view of the 2023 comprehensive results for the total industry (private carriers and state funds) will be presented at

AIS 2024, scheduled for May 13–15, 2024.

Notes

This document includes assumptions and projections. As with any prospective analysis, there exists estimation uncertainty in these assumptions and projections. Areas of this analysis subject to estimation uncertainty that could have a material impact on the results include:

- The development of Second Quarter 2023 DWP, DEP, and DIL to year-end values

- The relationship between direct and net business

- The expected expense ratios

- The impact of changes to laws and regulations

This article is provided solely as a reference tool to be used for informational purposes only. The information in this article shall not be construed or interpreted as providing legal or any other advice. Use of this article for any purpose other than as set forth herein is strictly prohibited.