KEY TAKEAWAYS

- Healthcare consolidation improves integration of care and reduces duplication of clinical services. Hospital mergers can lead to operating cost reductions for acquired hospitals of 15%−30%.

- Reductions in hospital operating costs do not translate into price decreases. Research to date shows that hospital mergers increase the average price of hospital services by 6%−18%.

- For Medicare, hospital concentration increases costs by increasing the

quantity of care rather than the

price of care.

- In addition to mergers, hospitals are also buying up provider practices. Between 2015 and 2016, hospitals acquired 5,000 physician practices.

- For workers compensation, hospital consolidation is likely to affect both the quantity and price of medical services. Forthcoming NCCI research will investigate the effect of hospital consolidation on prices

and utilization of medical services in workers compensation.

The Impact of Hospital Consolidation on Medical Costs

The year 2017 was a record one for merger and acquisition activity among hospitals and health systems, and this momentum is staying strong in 2018. This Drill Down describes the wave of hospital consolidation since 2010, identifies observed effects of hospital consolidation on utilization and prices of healthcare services, and discusses NCCI’s research in progress on the impact of hospital consolidation in workers compensation insurance.

Research to date has relied exclusively on data from commercial health insurance and Medicare in order to estimate impacts of hospital consolidation on utilization, costs, and outcomes. Of course, there are significant differences between these types of insurance and workers compensation. Medical services provided by commercial health insurance and Medicare are weighted toward prevention and treatment of chronic

diseases, whereas workers compensation focuses on treatment of

injuries. In addition, at least 35 states have adopted hospital fee schedules for workers compensation. Even so, the trend toward increasing hospital consolidation is likely to have produced similar upward pressures on utilization and price in workers compensation as those observed for other types of health insurance.

What Is Hospital Consolidation?

Consolidation in healthcare includes mergers, acquisitions, affiliation agreements, and facility closures. By combining former competitors in a market, consolidation has the potential to reduce competition, affect the

quantity of care, and increase prices. Most healthcare consolidation occurs through mergers and acquisitions involving two companies that provide similar ranges of healthcare services. A merger of companies producing services that are the same or close substitutes is a horizontal consolidation. Vertical consolidation, in contrast, refers to mergers of companies that produce upstream or downstream services within a production process—for example, a manufacturer’s acquisition of one of its suppliers or of a financial company that funds buyers of its products.

Horizontal Mergers and Acquisitions

Horizontal consolidation among hospitals is common and takes a variety of forms. The majority of merger and acquisition activity involves consolidation of individual hospitals into a hospital system. In other cases, hospitals are sold between hospital systems, or similar hospitals may join in a merger of equals. Large mergers can have important effects on local markets. One notable example is the merger of Beth Israel Deaconess Medical Center, Lahey Health, and several other hospital systems, which was approved by the Massachusetts’ Public Health Council in April 2018. Once completed, the combined hospital system will be the second largest healthcare system in Massachusetts, controlling nearly one-half of admissions in the state.

Vertical Acquisitions

Physicians do not compete with hospitals, but rather they provide services that are inputs to a hospital’s production of healthcare. The acquisition of physician practices by a hospital or hospital system is a common example of vertical consolidation in healthcare. Vertical consolidation also occurs when physician practices enter into formal affiliation agreements with hospitals while maintaining their separate ownership structure.

Recent Trends in Hospital Consolidation

Healthcare consolidation happens in waves. Largely as a response to the growth of managed care, the 1990s experienced an episode of “merger mania,” in which both hospitals and physician practices were rolled up into hospital systems.1 But by the early 2000s, hospital merger and acquisition activity had slowed and many of the acquired physician practices were divested.

We are now experiencing a second wave of healthcare consolidation that started around 2010. Between 2002 and 2009, announced hospital mergers and acquisitions averaged 55 deals per year. In 2011, there were 93 announced deals. Since then, 2017 was a

record year with 115 announced deals2 and 2018 has started at an even stronger pace with

30 announced transactions in the first quarter.3In 2007, approximately half (52.8%) of community hospitals belonged to a system; currently, two-thirds (66.8%) of community hospitals are in a system. Network participation by community hospitals has increased from 31% to 35% over the same period.4

Increased vertical consolidation has changed where physicians practice. Prior to 2009, more physicians practiced in

office-based settings rather than hospital-based settings. In 2005, approximately 50% of physicians practiced in a physician office; by 2015, only 40% of physicians are office-based. During the same period, the percent of hospital-employed physicians grew from 40% to 48% of all physicians.5

To understand how the healthcare marketplace is being transformed by consolidation, we separate hospital merger and acquisition activity into three types: 1) acquisition of other hospitals, 2) acquisition of provider practices, and 3) other forms of vertical integration (e.g., acquisition of ambulatory surgical centers or skilled nursing facilities).

In Figure 1, we show announced mergers in the hospital industry by these three categories, focusing only on activity by general medical and surgical hospitals.6 While the current wave of consolidation began in 2010, it has accelerated since 2014. Annual counts of acquisitions of hospitals and hospital systems have increased moderately since the 1990s, subject to fluctuations. But the number of acquisitions of provider practices doubled from 2013 and 2014 and have continued to increase since then. Likewise, hospital acquisitions of other entities such as community pharmacies, intermediate care facilities, and rehabilitation facilities jumped in 2015 and have stayed high in 2016 and 2017.

What Is Driving Hospital Consolidation?

The movement toward hospital consolidation since 2010 has been largely motivated by the

Affordable Care Act (ACA), the Medicare Access and CHIP Reauthorization Act (MACRA), and changing financial models.7 The ACA increased incentives to move patient care from an inpatient to an outpatient setting, motivating hospital systems to acquire physician practices in order to capitalize on increased outpatient revenues and secure referrals for hospital-based services. MACRA moves provider reimbursement from quantity of care to

quality of care. Improving quality measures is more difficult for solo and small provider practices. To improve reimbursement under MACRA, providers are increasingly joining large group and hospital-owned practices. The ACA encouraged the formation of Accountable Care Organizations (ACO) in the Medicare program.8 ACOs are groups of doctors, hospitals, and other healthcare providers that come together voluntarily to give coordinated high-quality care to their Medicare patients.

Compensation mechanisms for ACOs require that the ACO bear risk for patient or population outcomes, as opposed to receiving fees for service. Providers have financial incentives to consolidate into entities capable of providing integrated care. These financial incentives are driving the movement toward both horizontal and vertical consolidation among healthcare providers and changing market structure for the delivery of healthcare services.

A typical argument in favor of hospital consolidation is that efficiency improvements will result from economies of scale and eliminate redundant services. In addition, improvements in quality of care are possible through enhanced care coordination and sustained capital investment to expand clinical services. Stroke intervention and post-stroke care are examples of how hospital consolidation can improve outcomes and potentially reduce costs.

A hospital with integrated rehabilitation would likely begin physical and occupational therapy during the initial hospital stay and then coordinate with outpatient rehabilitation. Without an integrated rehabilitation unit, the hospital would discharge patients and refer them elsewhere for rehabilitation. Even though the initial hospital stay may have higher costs, early intervention and improved care coordination might enhance the efficacy of care and reduce the length of rehabilitation—resulting in overall lower costs to insurance carriers.

Hospitals emphasize that increasing the number of patients served and services delivered decreases the average cost of service because of scale economies. Besides reducing administrative costs, a merger of two hospitals organizes patient care under a common operating model. In addition, a merger can standardize clinical processes and referrals and eliminate overlapping service lines. Hospital mergers can lead to

cost reductions of 15% to 30%9 from economies of scale. After merging into a larger hospital system, smaller hospitals often make

substantial capital investments.10 Because small independent hospitals have tight operating margins and limited access to capital markets, mergers into larger hospital networks

provides access to capital.11

Advocates of hospital mergers, particularly the merging hospitals themselves, emphasize efficiency and scale advantages such as those described above. However, research to date on completed hospital mergers has yet to demonstrate the benefits of consolidation via improved quality, access, and cost. Mergers increase the

likelihood of intensive surgery and total number of surgeries, but do not improve patient outcomes.12 Mergers have also been found to

reduce hospital costs per risk-adjusted discharge, but not to reduce the price of hospital care to insurers.13

Other studies study the level of competition rather than mergers per se and find positive effects of competition on patients. A 2012 review of studies using American and English data found that competition

improves access and mortality.14 A study on the effects of six medical conditions in California found that increased competition

improves 30-day mortality.

How Does Hospital Consolidation Affect Competition?

Hospital consolidation presents a tradeoff. Even if a merger is motivated by network and cost efficiencies, it can also increase market

power for the merged hospital system. Assessing the effects of a proposed hospital acquisition on the performance of healthcare markets requires asking some basic but difficult questions:

- What is the relevant healthcare services market that is affected by the proposed acquisition?

- How competitive is the relevant healthcare services market before the proposed acquisition?

- How much of an incremental impact on competition is the proposed acquisition likely to have—especially on the power of the merged entity to influence utilization and pricing?

In fact, these three questions are central to merger reviews as conducted by US antitrust authorities at the Department of Justice and Federal Trade Commission. Merger review from an antitrust perspective is explicitly concerned with the potential increase in market leverage and pricing

power, not about the reduction in the number of competitors

per se. Over decades of practice, US antitrust authorities have developed a systematic way of thinking about the competitive effects of market consolidation, as well as some specific guidelines for answering the questions posed above.

What Are the Relevant Markets in Which Hospitals Compete?

To evaluate the competitive impact of a proposed hospital merger, antitrust authorities begin by identifying the relevant regional market for hospital services. Among the factors considered in defining a regional hospital market are distance between hospitals, clinical capabilities, population size, and local legal restrictions. Hospitals and other providers in a region have naturally existing referral patterns for primary, acute, and specialty medical care. Small hospitals often do not have the patient base to support specialist services such as oncology, cardiology, and orthopedic surgery. In a typical regional market, small hospitals serve as referral sources to large urban hospitals that provide an array of specialties.

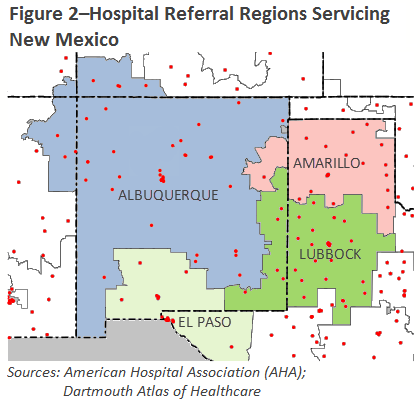

The

Hospital Referral Region (HRR) is a popular geographic specification for regional hospital markets. The HRR concept was developed by the Dartmouth Atlas from Medicare data in order to capture referral patterns in primary, secondary, and tertiary care. Each HRR must have a tertiary referral hospital for major procedures such as cardiovascular and neurosurgical surgery.

The geographic size of an HRR and the distribution of hospitals in it are key elements in assessing the market’s competitiveness and the potential impacts of consolidation. For illustration, New Mexico is a large rural state that is primarily served by the Albuquerque HRR. As shown in Figure 2, the Albuquerque HRR extends into northeastern Arizona and southwestern Colorado. A southern section of New Mexico is in the El Paso HRR, and eastern sections are divided into the Amarillo and Lubbock HRRs. There are several metropolitan areas in New Mexico that serve as cardiovascular referral centers, but only Albuquerque has the capacity for major neurosurgical procedures.

US antitrust authorities use the

Herfindahl-Hirschman Index (HHI) as an indicator for markets in which suppliers are concentrated, and where a proposed merger might have a significant competitive impact. The HHI is calculated by summing the squared product shares (expressed in whole numbers) for all competitors in a market. The HHI for a monopoly market with only one hospital is 10,000 (= 100 x 100). Similarly, a market in which one hospital has a 40% share of admissions and six other hospitals have 10% each has an HHI of 2,200.

By

US Department of Justice Horizontal Merger Guidelines, a market with an HHI of:

- Greater than 2,500 is considered highly concentrated

- Between 1,500 and 2,500 is considered moderately concentrated

- Below 1,500 is considered unconcentrated

The HHI is a useful indicator to assess the extent of market concentration in an existing market, as well the change in market concentration from a proposed merger. By itself, the HHI does not provide a definitive answer to the question of how much a proposed merger will impact utilization and pricing in the relevant market. These economic outcomes will depend on other factors going beyond the pre-merger market shares of healthcare providers. Rather, the purpose of the HHI is to draw attention to hospital markets and mergers in which competitiveness may be at risk because of high concentration among suppliers, and to signal the need for closer analysis.

Returning to the New Mexico example, the Albuquerque HRR contains 37 hospitals, of which the two largest have 25% and 17% of hospital admissions. Its HHI is 1,175 and is therefore considered to be a competitive market. The Albuquerque HRR is typical of a rural-serving HRR. Urban areas have much greater variance with respect to concentration. The Houston (TX) HRR has 65 hospitals and an HHI of 394 (very unconcentrated). The Paterson (NJ) HRR has two hospitals, with one having 88% market share, and an HHI of 7,888 (very concentrated). In the Houston HRR, if any two hospitals merged, the HRR would still be considered competitive; but this is not true for the Paterson HRR.

How Concentrated Are Hospital Markets?

Hospital market concentration has been increasing over time. Figure 3 maps the hospital concentration by HRR from the CMS Provider of Service (POS) files in 2000 and 2017. The HHI was calculated by share of total hospital beds for general medical and surgical hospitals. The areas in red represent HRRs with relatively high market concentration as defined by an HHI greater than 2,500. The average HHI in 2000 was 2,054, increasing to 2,676 by 2017. In 2000, 30% of HRRs had an HHI greater than 2,500, but by 2017 44% of HRRs were above this level.

Highly concentrated HRRs have an average of four hospitals, while the less concentrated HRRs have an average of 16 hospitals. Rural HRRs tend to be much larger and less concentrated than urban HRRs. This is largely because rural HRRs’ referral hospitals serve many small hospitals over an extensive geographic region, whereas urban HRRs’ referral hospitals are supported by fewer (and larger) hospitals in smaller geographic regions.

What Is the Evidence to Date on the Price Impacts of Hospital Consolidation?

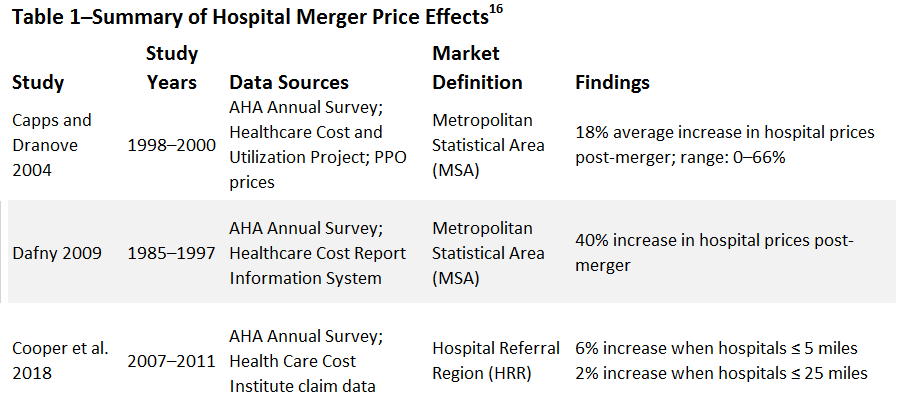

Recent research shows that hospital concentration increases prices paid by commercial insurers. The extent of the price impact depends on the definition of the market, time frame of the study, and payers of care. Table 1 summarizes the findings of three recent studies. The largest price impact (40% increase in price) used the Healthcare Cost Report Information System (HCRIS) and calculated an average price for all payers as the inpatient revenue per case-mix adjusted discharge. The middle estimate of 18% increase used negotiated provider prices pre- and post-merger. Both studies defined the relevant hospital market by metropolitan statistical area. The smallest effect of a 6% increase for mergers with nearby hospitals was based on health insurance data from four insurers.

All three studies focused primarily or exclusively on

inpatient prices.

Medicare provides an interesting counterpoint. Research such as Cooper et al., shows that hospital concentration increases the cost of care for Medicare fee-for-service (FFS), but in contrast to commercial insurance, this occurs by increasing the

quantity of care rather than the price of care. In more concentrated markets, there is an increased likelihood of being discharged to a post-acute care facility rather than discharged to home, the use of inpatient rather than outpatient surgery is higher, and there is an increase in the number of inpatient admissions for the same level of acuity.17 Medicare FFS has a fixed fee schedule, so hospitals cannot negotiate the price of services. However, Medicare FFS patients in more concentrated hospital markets do receive more services than those in less concentrated markets. This result is not surprising, since more concentrated hospital systems have a greater ability to provide intensive high-fee services in-house, rather than referring them out.

As with hospital consolidation, provider concentration has been found to increase the cost of services. Vertical integration increases the costs of services for two reasons. When hospitals own provider practices, the hospital can charge a facility fee in addition to the providers’ professional reimbursement. A recent study found vertical integration

increased hospital outpatient prices by 14%, with a quarter of that increase due to facility fees.18

NCCI’s Forthcoming Research on Hospital Consolidation

To date, there has been no study on the impacts of healthcare consolidation on workers compensation. Impacts of hospital concentration have been estimated for commercial health insurance and Medicare, which can help explain the effect on workers compensation even though the types of care are different. It is likely that the price of inpatient services for workers compensation is higher in highly concentrated markets and, like Medicare, that higher quantities of medical services are provided.

Forthcoming research by NCCI will use the Medical Data Call to address these questions:

- How much do prices paid in workers compensation for hospital-based medical care vary for related diagnoses between different regional markets for hospital services?

- What is the impact of concentration in regional markets for hospital services on prices paid in workers compensation for hospital-based medical care after controlling for patient severity and hospital characteristics such as ownership, size, medical school affiliation, and wage variance?

This article is provided solely as a reference tool to be used for informational purposes only. The information in this article shall not be construed or interpreted as providing legal or any other advice. Use of this article for any purpose other than as set forth herein is strictly prohibited.